Trading in the financial market is a daunting task in spite of the attracting increase of the daily turnover of the Forex financial market from 6.5 trillion USD in 2022 to approximately 7.5 trillion USD in 2024. About 80% of retail investors lose money. However, to minimize the risk of losses, investors explore the possibility of profitable trading by resorting to social trading. In social trading of the financial market, the performance statistics and performance charts of traders with diverse trading strategies, methods and characteristics are showcased by the financial market brokers to enable investors decide on which trader’s signal to adopt or copy for profitable investment. However, investors are often faced with the problem of choosing a set of profitable traders among thousands with different past hypothetical results, in spite of the provision of traders’ performance ranking, made available by the brokers. The investors have serious concern on the stability, sustainability and predictability of a trader’s future performance which will eventually determine the investors profit or loss if the trader’s signals are copied or followed. This paper applies three deep learning models: the multilayer perceptron, recurrent neural network and long short term memory for the prediction of traders’ profitability to provide the best model for investment in the financial market, and reports the experience. The results of the study show that recurrent neural network performs best, followed by long short term memory while multilayer perceptron yields the least results for the prediction. These three models yield a mean squared error of 0.5836, 0.7075 and 0.9285 respectively in a test scenario for a trader.

| Published in | American Journal of Computer Science and Technology (Volume 7, Issue 2) |

| DOI | 10.11648/j.ajcst.20240702.14 |

| Page(s) | 51-61 |

| Creative Commons |

This is an Open Access article, distributed under the terms of the Creative Commons Attribution 4.0 International License (http://creativecommons.org/licenses/by/4.0/), which permits unrestricted use, distribution and reproduction in any medium or format, provided the original work is properly cited. |

| Copyright |

Copyright © The Author(s), 2024. Published by Science Publishing Group |

Deep Learning, Traders, Financial Market, Performance, Prediction

Broker Ticket | Type | Currency | Date Open | Price Open | Price Close | Profit (pips) |

|---|---|---|---|---|---|---|

65207563 | SELL | EUR/USD | 2019/05/28 | 2019/05/29 | 1.11623 | 1.11519 |

65252549 | SELL | EUR/USD | 2019/05/29 | 2019/05/29 | 1.11521 | 1.11521 |

65417368 | SELL | EUR/USD | 2019/05/29 | 2019/05/30 | 1.11332 | 1.11281 |

65739566 | BUY | EUR/USD | 2019/05/30 | 2019/05/31 | 1.11299 | 1.1135 |

66859276 | SELL | EUR/USD | 2019/06/13 | 2019/06/14 | 1.12765 | 1.12706 |

66958990 | SELL | EUR/USD | 2019/06/16 | 2019/06/17 | 1.12112 | 1.12054 |

Trained Data | Test Data | |||||

|---|---|---|---|---|---|---|

Trader/Model | RMSE | MAPE |

| RMSE | MAPE |

|

A/MLP | 0.1532 | 0.2114 | 0.9765 | 0.9285 | 0.3935 | -10.0325 |

A/RNN | 0.0500 | 0.0674 | 0.9975 | 0.5836 | 0.2407 | -3.4326 |

A/LSTM | 0.5050 | 0.0902 | 0.9974 | 0.7075 | 0.2949 | -5.5135 |

B/MLP | 0.0987 | 0.1270 | 0.9903 | 1.5025 | 0.4254 | -23.2741 |

B/RNN | 0.0444 | 0.0701 | 0.9980 | 0.6565 | 0.2099 | -3.7806 |

B/LSTM | 0.0400 | 0.0562 | 0.9984 | 0.7890 | 0.2591 | -5.9056 |

C/MLP | 0.1898 | 0.6375 | 0.9640 | 4.5808 | 0.5211 | -5.6889 |

C/RNN | 0.1014 | 0.1940 | 0.9897 | 3.7826 | 0.4646 | -3.6175 |

C/LSTM | 0.1067 | 0.3320 | 0.9886 | 3.9640 | 0.4928 | -4.0711 |

MC | Machine Learning |

NN | Neural Network |

RNN | Recurrent Neural Network |

LSTM | Long Short-Term Memory |

MLP | Multilayer Perceptron |

DMLP | Deep Multilayer Perceptron Models |

DL | Deep Learning |

RMSE | Root Mean Squared Error |

MAPE | Mean Absolute Percentile Error |

| [1] | Oyemade, D. A., Ojugo, A. A. An optimized input genetic algorithm model for the financial market. International Journal of Innovative Science, Engineering & Technology. 2021, 8 (2), 408-419. |

| [2] | Abdul Lateef A. A., Sufyan, T., Al-Janabi, S. T. F., Al-Khateeb, B. Survey on intrusion detection systems based on deep learning. Periodicals of Engineering and Natural Sciences 2019. 7 (3), pp. 1074-1095. |

| [3] | Sezer, O. B., Gudelek, M. U., Ozbayoglu, A. M. Financial time series forecasting with deep learning: a systematic literature review: 2005–2019. Applied Soft Computing Journal. 2020, 90 (106181), pp. 1-27. |

| [4] | Goodfellow, I., Bengio, Y., Courville, A. Deep Learning; 2016, MIT Press. |

| [5] | Cybenko, G. Approximation by superpositions of a sigmoidal function. Math. Control Signals Systems. 1989, 2 (4), pp. 303–314. |

| [6] | Kalman, B. L., Kwasny, S. C. Why tanh: choosing a sigmoidal function. In Proceedings of IJCNN International Joint Conference on Neural Networks, Baltimore, MD, USA. 1992; pp. 578–581. |

| [7] | Nair, V., Hinton, G. E. Rectified linear units improve restricted Boltzmann machines. In Proceedings of the 27th International Conference on Machine Learning. 2010; pp. 807–814. |

| [8] | Maas, A. L., Hannun, A. Y., Ng, A. Y. Rectifier nonlinearities improve neural network acoustic models. In Proceedings of the 30th International Conference on Machine Learning, Atlanta. 2013; pp. 3. |

| [9] | Bengio Y., Simard, P., Frasconi, P. Learning long-term dependencies with gradient descent is difficult. IEEE Transactions on Neural Networks. 1994, 5(2), pp. 157–166. |

| [10] | Hochreiter, S., Schmidhuber, J., Long short-term memory. Neural Computation. 1997, 9(8), pp. 1735–1780. |

| [11] | Greff, K., Srivastava, R. K., Jan, K. J., Steunebrink, B. R., Schmidhuber, J. LSTM: A search space odyssey. IEEE Transanctions on Neural Networks and Learning Systems. 2016, 28 (10), pp. 2222–2232. |

| [12] | Kasongo, S. M., Sun, Y. A deep learning method with filter based feature engineering for wireless intrusion detection system. IEEE Access. 2019, 7 (2019), pp. 38597–38607. |

| [13] | Tariq, M. I., Memon, N. A., Ahmed, S., Tayyaba, S., Mushtaq, M. T. et al. A review of deep learning security and privacy defensive techniques. Hindawi Mobile Information Systems, 2020, 2020, pp. 18. |

| [14] | Sehovac, L., Grolinger, K. Deep learning for load forecasting: sequence to sequence recurrent neural networks with attention. IEEE Access. 2020, 8 (2020), pp. 36411-36426. |

| [15] | Joseph, J., Aswin, R., James, A., Johny, A., Jose, P. V. Smart waste management using deep learning with IoT. International Journal of Networks and Systems. 2019, 8 (3), pp. 37–40. |

| [16] | Gayathri, M., Meghana, M., Trivedh, M., Manju, D. Suspicious activity detection and tracking through unmanned aerial vehicle using deep learning techniques. International Journal of Advanced Trends in Computer Science and Engineering. 2020, 9 (3), pp. 2812-2816. |

| [17] | Fang, X., Xu, M., Shouhuai, Xu, S., Zhao, P. A deep learning framework for predicting cyber attacks rates. EURASIP Journal on Information Security. 2019, 5, pp. 11. |

| [18] | Vogl, M., Rötzel, P. R., Homes, S. Forecasting performance of wavelet neural networks and other neural network topologies: A comparative study based on financial market data sets. Machine Learning with Applications. 2022, 8 (100302), 1-13. |

| [19] | Schmidt-Kessen M. J., Eenmaa, H, Mitre, M. Machines that make and keep promises - Lessons for contract automation from algorithmic trading on financial markets. Computer Law and Security Review. 2022, 46 (105717), 1-17. |

| [20] | Zhang, H. Optimization of risk control in financial markets based on particle swarm optimization algorithm. Journal of Computational and Applied Mathematics. 2020, 368 (112530), 1-12. |

| [21] | Dash, R. Performance analysis of an evolutionary recurrent legendre polynomial neural network in application to forex prediction. Journal of King Saud University – Computer and Information Sciences. 2020, 32, 1000-1011. |

| [22] | Supsermpol, P., Huynh, V, N., Thajchayapong, S., Chiadamrong, N. Predicting financial performance for listed companies in Thailand during the transition period: A class-based approach using logistic regression and random forest algorithm. Journal of Open Innovation: Technology, Market, and Complexity. 2023, 9 (100130), 1-16. |

| [23] | Ueda, K., Suwa, H., Yamada, M., Ogawa, Y., Umehara, E. et al. SSCDV: Social media document embedding with sentiment and topics for financial market forecasting. Expert Systems with Applications. 2024, 245 (122988), 1-16. |

| [24] | Oyemade, D. A., Ekuobase, G. O., Chete, F. O. Fuzzy logic expert advisor topology for foreign exchange market. In Proceedings of the International Conference on Software Engineering and Intelligent Systems, Covenant University, Otta, Nigeria. 2010; pp. 215–227. |

| [25] | Bevilacqua, M., Tunaru, R., Vioto, D. Options-based systemic risk, financial distress, and macroeconomic downturns. Journal of Financial Markets. 2023, 65 (100834), pp. 1-35. |

| [26] | Bossaerts, F., Yadav, N., Bossaerts, P., Nash, C., Todd, T. et al. Price formation in field prediction markets: The wisdom in the crowd. Journal of Financial Markets. 2024, 68 (100881), pp. 1-16. |

| [27] | Allenotor, D., Oyemade, D. A. A price-based grid resources pricing approach for non-storable real assets. Journal of Advances in Mathematical & Computational Science. 2022, 10 (2), 1-18. |

| [28] | Allenotor, D., Oyemade, D. A. An optimized parallel hybrid architecture for cryptocurrency mining. Computing, Information Systems, Development Informatics & Allied Research Journal. 2022, 12 (1), 94-104. |

| [29] | Oyemade, D. A., Enebeli D. A dynamic level technical indicator model for oil price forecasting. Global Journal of Computer Science and Technology, 2021, 21 (1), 5-14. |

| [30] | Oyemade DA, Allenotor D. A quality of service (QoS) model for forex brokers’ platforms. International Journal of Innovative Science, Engineering & Technology, 2022, 9 (6), 123-132. |

| [31] | Gündüz, H., Zehra, C.¸ Çataltepe, Z., Yaslan Z. Stock daily return prediction using expanded features and feature selection. Turkish Journal of Electrical Engineering and Computer Sciences. 2017, 25 (6), 4829-4840. |

| [32] | Altuner, A. B., Kilimci, Z. H. A novel deep reinforcement learning based stock price prediction using knowledge graph and community aware sentiments. Turkish Journal of Electrical Engineering and Computer Sciences 2022; 30 (4), pp. 1506 – 1524. |

| [33] | Oyemade, D. A., Allenotor, D. FAITH software life cycle model for forex expert advisors. Journal of Advances in mathematical and Computational Sciences 2021; 9 (1): 1-12. |

| [34] | Oyemade, D. A. A typified greedy dynamic programming model for the metatrader platform. Journal of Advances in Mathematical and Computational Sciences. 2020, 8 (3): 49-60. |

| [35] | Oyemade, D. A., Ojugo, A. A. A property oriented pandemic surviving trading model. International Journal of Advanced Trends in Computer Science and Engineering. 2029, 9 (5), 7397-7404. |

| [36] | Oyemade, D. A., Allenotor, D. A Trade gap scalability model for the forex market. In IEEE 11th International Conference on Ubiquitous Intelligence & Computing and IEEE 11th International Conference on Autonomic & Trusted Computing; Washington, DC, USA. 2014; pp. 867 – 873. |

| [37] | Dezsi, E., Nistor, I. A. Can deep machine learning outsmart the market? A comparison between econometric modelling and long- short term memory. Romanian Economic and Business Review. 2016, 11 (41), pp. 54–73. |

| [38] | Almeida, B. J., Neves, R. F., Horta, N. Combining support vector machine with genetic algorithms to optimize investments in forex markets with high leverage. Applied Soft Computing. 2018, 64 (2018), pp. 596–613. |

| [39] | Nia, L., Li, Y., Wang, X., Zhaing, J., Yud, J. Forecasting of forex time series data based on deep learning. Procedia Computer Science. 2019, 147 (2019), pp. 647–652. |

| [40] | Carapuço, J., Neves, R., Horta, N. Reinforcement learning applied to forex trading. Applied Soft Computing Journal. 2018, 73 (2018), pp. 783–794. |

| [41] | Kingman, D. B., Ba, L. J. Adam: A method for stochastic optimization. In Proceedings of the International Conference on Learning Representations; San Diego, CA, USA. 2015; pp. 13. |

| [42] | Ballester, R., Clemente, X. A., Casacuberta, C., Madadi, M., Corneanu, C. A., Sergio Escalera, S. Predicting the generalization gap in neural networks using topological data analysis, Neurocomputing. 2024, 596(127787), pp. 1-14. |

| [43] | Jia, D., Liwei Yang, L., Lv, T., Weiping Liu, W., Gao, X., Zhou, J. Evaluation of machine learning models for predicting daily global and diffuse solar radiation under different weather/pollution conditions. Renewable Energy. 2022, 187, pp. 896-906. |

| [44] | McHale, I. G., Holmes, B. Estimating transfer fees of professional footballers using advanced performance metrics and machine learning. European Journal of Operational Research. 2023, 306(1), pp. 389-399. |

| [45] | Jain, P., Islam, M. T., Ahmed S. Alshammari, A. S. Comparative analysis of machine learning techniques for metamaterial absorber performance in terahertz applications. Alexandria Engineering Journal. 2024, 103, pp. 51-59. |

APA Style

Oyemade, D. A., Ben-Iwhiwhu, E. (2024). An Investigation of Predictability of Traders' Profitability Using Deep Learning. American Journal of Computer Science and Technology, 7(2), 51-61. https://doi.org/10.11648/j.ajcst.20240702.14

ACS Style

Oyemade, D. A.; Ben-Iwhiwhu, E. An Investigation of Predictability of Traders' Profitability Using Deep Learning. Am. J. Comput. Sci. Technol. 2024, 7(2), 51-61. doi: 10.11648/j.ajcst.20240702.14

AMA Style

Oyemade DA, Ben-Iwhiwhu E. An Investigation of Predictability of Traders' Profitability Using Deep Learning. Am J Comput Sci Technol. 2024;7(2):51-61. doi: 10.11648/j.ajcst.20240702.14

@article{10.11648/j.ajcst.20240702.14,

author = {David Ademola Oyemade and Eseoghene Ben-Iwhiwhu},

title = {An Investigation of Predictability of Traders' Profitability Using Deep Learning

},

journal = {American Journal of Computer Science and Technology},

volume = {7},

number = {2},

pages = {51-61},

doi = {10.11648/j.ajcst.20240702.14},

url = {https://doi.org/10.11648/j.ajcst.20240702.14},

eprint = {https://article.sciencepublishinggroup.com/pdf/10.11648.j.ajcst.20240702.14},

abstract = {Trading in the financial market is a daunting task in spite of the attracting increase of the daily turnover of the Forex financial market from 6.5 trillion USD in 2022 to approximately 7.5 trillion USD in 2024. About 80% of retail investors lose money. However, to minimize the risk of losses, investors explore the possibility of profitable trading by resorting to social trading. In social trading of the financial market, the performance statistics and performance charts of traders with diverse trading strategies, methods and characteristics are showcased by the financial market brokers to enable investors decide on which trader’s signal to adopt or copy for profitable investment. However, investors are often faced with the problem of choosing a set of profitable traders among thousands with different past hypothetical results, in spite of the provision of traders’ performance ranking, made available by the brokers. The investors have serious concern on the stability, sustainability and predictability of a trader’s future performance which will eventually determine the investors profit or loss if the trader’s signals are copied or followed. This paper applies three deep learning models: the multilayer perceptron, recurrent neural network and long short term memory for the prediction of traders’ profitability to provide the best model for investment in the financial market, and reports the experience. The results of the study show that recurrent neural network performs best, followed by long short term memory while multilayer perceptron yields the least results for the prediction. These three models yield a mean squared error of 0.5836, 0.7075 and 0.9285 respectively in a test scenario for a trader.

},

year = {2024}

}

TY - JOUR T1 - An Investigation of Predictability of Traders' Profitability Using Deep Learning AU - David Ademola Oyemade AU - Eseoghene Ben-Iwhiwhu Y1 - 2024/07/08 PY - 2024 N1 - https://doi.org/10.11648/j.ajcst.20240702.14 DO - 10.11648/j.ajcst.20240702.14 T2 - American Journal of Computer Science and Technology JF - American Journal of Computer Science and Technology JO - American Journal of Computer Science and Technology SP - 51 EP - 61 PB - Science Publishing Group SN - 2640-012X UR - https://doi.org/10.11648/j.ajcst.20240702.14 AB - Trading in the financial market is a daunting task in spite of the attracting increase of the daily turnover of the Forex financial market from 6.5 trillion USD in 2022 to approximately 7.5 trillion USD in 2024. About 80% of retail investors lose money. However, to minimize the risk of losses, investors explore the possibility of profitable trading by resorting to social trading. In social trading of the financial market, the performance statistics and performance charts of traders with diverse trading strategies, methods and characteristics are showcased by the financial market brokers to enable investors decide on which trader’s signal to adopt or copy for profitable investment. However, investors are often faced with the problem of choosing a set of profitable traders among thousands with different past hypothetical results, in spite of the provision of traders’ performance ranking, made available by the brokers. The investors have serious concern on the stability, sustainability and predictability of a trader’s future performance which will eventually determine the investors profit or loss if the trader’s signals are copied or followed. This paper applies three deep learning models: the multilayer perceptron, recurrent neural network and long short term memory for the prediction of traders’ profitability to provide the best model for investment in the financial market, and reports the experience. The results of the study show that recurrent neural network performs best, followed by long short term memory while multilayer perceptron yields the least results for the prediction. These three models yield a mean squared error of 0.5836, 0.7075 and 0.9285 respectively in a test scenario for a trader. VL - 7 IS - 2 ER -

Department of Computer Science, Federal University of Petroleum Resources, Effurun, Nigeria

Biography: David Ademola Oyemade is an Associate Professor of Computer Science at the Federal University of Petroleum Resources, Effurun, Delta State, Nigeria. He holds a PhD degree in Computer Science obtained from the University of Benin, Benin City, Nigeria in 2014. He also holds M.Sc. degree in Computer Science obtained from the University of Benin, Benin City, Nigeria in 2007 and a postgraduate diploma in Computer Science obtained from the University of Benin, Benin City, in 2004. He is a life member of Nigeria Computer Society (NCS) and a professional member of Association for Computing Machinery (ACM). He has served as a lecturer in the Department of Computer Science, Federal University of Petroleum Resources, Effurun and rose through various ranks. He has supervised several students at undergraduate and postgraduate levels at the department of Computer Science, Federal University of Petroleum Resources, Effurun. He has many articles in international and local journals. His research area is Software Engineering, Software Architecture, Intelligent Systems and financial market algorithms and modelling.

Research Fields: Software Engineering, Software Architecture, Intelligent Software Systems, Financial Market Algorithms, Deep Learning

Department of Computer Science, Federal University of Petroleum Resources, Effurun, Nigeria

Biography: Eseoghene Ben-Iwhiwhu holds a PhD degree from Loughborough University, United Kingdom (UK). He also holds an M.Sc. and B.Sc. degrees from Coventry University, UK and the Federal University of Petroleum Resources Effurun. He is an assistant lecturer in the department of Computer Science, Federal University of Petroleum Resources Effurun. His research interest includes machine learning, deep learning, reinforcement learning, Hebbian learning and neuroevolution.

Research Fields: Machine Learning, Deep Learning, Reinforcement Learning, Hebbian Learning and Neuroevolution

Figure 2. Feature encoding using a pandas dataframe.

Figure 3. Graphical representations of the deep learning models.

Figure 4. Actual values and trained prediction plots for Trader B.

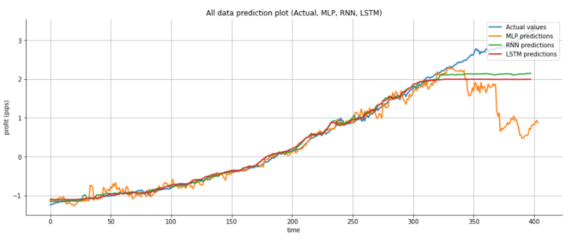

Figure 5. Trained and test data prediction plots for trader A.

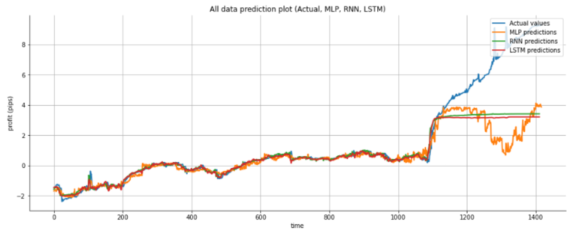

Figure 6. Trained and test data prediction plots for trader B.

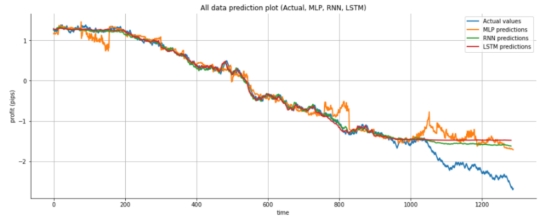

Figure 7. Trained and test data prediction plots for trader C.

Information