1. Introduction

1.1. The Problem: When Data Is Not Enough

Banks today are not constrained by a lack of data. On the contrary, they operate in environments saturated with signals, interactions, and behavioral traces. Yet despite this abundance, a structural gap persists between data availability and value creation. The limitation is not primarily technological, but conceptual.

For decades, banks have relied on deterministic frameworks to interpret customer behavior. Segmentation models, channel attribution logic, and static classifications assume that customers are stable, observable, and ultimately classifiable into predefined categories.

These assumptions are increasingly inadequate in contemporary contexts.

This limitation is widely documented in the literature on digital transformation, omnichannel behavior, and customer experience

| [3] | Naldi, F. (2023). Economia comportamentale: principi base e applicazioni. State of Mind. |

| [7] | Brynjolfsson, E., & McAfee, A. (2017). The Business of Artificial Intelligence. Harvard Business Review. |

| [8] | Verhoef, P. C., Kannan, P. K., & Inman, J. J. (2015). From Multi-channel Retailing to Omni-channel Retailing. Journal of Retailing, 91(2), 174-181.

https://doi.org/10.1016/j.jretai.2015.02.005 |

| [9] | Lemon, K. N., & Verhoef, P. C. (2016). Understanding Customer Experience. Journal of Marketing, 80(6), 69-96.

https://doi.org/10.1509/jm.15.0420 |

[3, 7-9]

.

Customers are inherently dynamic systems, moving across channels, shifting intentions, and evolving in non-linear ways. A customer may explore digitally, evaluate cognitively, disengage temporarily, and re-enter through a relational interaction.

Capturing such behavior through fixed segments is not only insufficient—it is misleading.

1.2. The White-Out Syndrome: Why Channel-Based Classification Fails

One of the most persistent flaws in traditional customer models is the tendency to classify customers into rigid categories such as “digital” or “physical.” While intuitively appealing, this distinction introduces a critical distortion: it assumes that behavior is stable, observable, and reducible to a single dominant state.

Empirical evidence suggests otherwise.

Modern customers do not exist as purely digital or physical entities, as also highlighted in research on omnichannel customer behavior

| [7] | Brynjolfsson, E., & McAfee, A. (2017). The Business of Artificial Intelligence. Harvard Business Review. |

| [8] | Verhoef, P. C., Kannan, P. K., & Inman, J. J. (2015). From Multi-channel Retailing to Omni-channel Retailing. Journal of Retailing, 91(2), 174-181.

https://doi.org/10.1016/j.jretai.2015.02.005 |

[7, 8]

. They move continuously across contexts, channels, and levels of engagement. Attempting to fix them into one category does not simplify complexity—it obscures it.

This phenomenon can be described as a “white-out syndrome.”

In aviation, a white-out occurs when visual references disappear: sky and ground blend into a uniform field, the horizon vanishes, and spatial orientation is lost. The danger lies not only in disorientation, but in the illusion that control still exists.

A similar phenomenon can be observed in customer interpretation.

When banks persist in classifying customers as “digital” or “physical,” they lose the ability to distinguish trajectories, intentions, and decision moments. Data continues to flow, interactions continue to occur—but the underlying behavior becomes opaque.

The problem is not that customer behavior becomes more complex. The problem is that the model used to interpret it becomes blind.

In an environment characterized by hybrid, non-linear behavior, channel-based classification creates a false sense of clarity while progressively eroding visibility.

The QS Cube is designed to restore that visibility. Instead of reducing the customer to a category, it represents behavior as a probabilistic trajectory—making patterns observable again within an otherwise indistinguishable landscape.

Key Insight

Value does not originate from the channel. It emerges from the intersection of engagement and decision.

From Deterministic Customers to Probabilistic Systems

To address this gap, the QS Cube (Quantum Superposition Customer Behavior®) introduces a different conceptual foundation.

Registered as a proprietary trademark at the European Union Intellectual Property Office (EUIPO), the model reframes the customer as a probabilistic system.

Instead of a fixed state, the customer exists as a distribution of possible states.

2. Theoretical Framework

The Physics Behind the Model: From Metaphor to Structure

The quantum analogy embedded in the QS Cube is not intended as a superficial metaphor, but as a structured interpretive framework for systems characterized by uncertainty, non-linearity, and contextual dependence. Similar approaches have been explored in the emerging field of quantum economics and decision theory, where probabilistic models extend beyond classical deterministic assumptions

| [1] | Holtfort, T., & Horsch, A. (2024). Quantum Economics: A Systematic Literature Review. FOM University Press. |

| [17] | Khrennikov, A. (2010). Ubiquitous Quantum Structure: From Psychology to Finance. Springer. |

[1, 17]

.

In quantum mechanics, the principle of superposition states that a system can exist simultaneously in multiple states until it is observed

| [16] | Dirac, P. A. M. (1930). The Principles of Quantum Mechanics. Oxford University Press. |

[16]

, a structured interpretative framework.

This concept provides a useful analytical lens to interpret modern customer behavior. Customers do not occupy a single behavioral state at a given moment; instead, they exist across multiple potential states that coexist probabilistically

| [2] | Maksymov, I. S. (2025). Cognition in Superposition: Quantum Models in AI, Finance, Defence, Gaming and Collective Behaviour. Charles Sturt University. |

[2]

.

This perspective aligns with developments in behavioral economics, which highlight the non-linear, context-dependent nature of human decision-making

| [4] | Kahneman, D. (2011). Thinking, Fast and Slow. New York: Farrar, Straus and Giroux. |

| [5] | Thaler, R. H. (2015). Misbehaving: The Making of Behavioral Economics. W. W. Norton & Company. |

[4, 5]

. However, while behavioral economics explains deviations from rationality, the QS Cube introduces a structural representation of uncertainty itself.

The modeling of customer behavior through a wave function ψ(s) reflects this probabilistic nature. The squared magnitude of this function represents the likelihood of observing a specific customer action. While not intended as a strict mathematical formalization, this representation clarifies that behavior is inherently probabilistic rather than deterministic

| [18] | Busemeyer, J. R., & Bruza, P. D. (2012). Quantum Models of Cognition and Decision. Cambridge University Press. |

[18]

.

The concept of “measurement” further reinforces this framework. In quantum systems, observation alters the state of the system. Similarly, every interaction with a customer—whether digital, automated, or human—modifies the probability distribution of future behavior

| [6] | Davenport, T. H., & Ronanki, R. (2018). Artificial Intelligence for the Real World. Harvard Business Review, 96(1), 108-116. |

[6]

.

The moment of decision can therefore be interpreted as a collapse of the probability distribution, where uncertainty resolves into a single observable outcome. This aligns with emerging discussions on probabilistic cognition and decision dynamics

| [2] | Maksymov, I. S. (2025). Cognition in Superposition: Quantum Models in AI, Finance, Defence, Gaming and Collective Behaviour. Charles Sturt University. |

[2]

.

From a managerial perspective, this implies a fundamental shift: organizations do not manage customers as fixed entities, but as evolving probability distributions. Consequently, value is not generated continuously, but emerges discontinuously at the moment of decision, when probabilistic potential is converted into observable behavior

.

2.1. Superposition

Superposition: Multiple States Coexist

In quantum mechanics, a system does not occupy a single state until it is observed. Instead, it exists in a superposition of possible states, each associated with a probability amplitude.

Similarly, a customer is never in a single, stable condition.

At any given moment, an individual may simultaneously explore digitally, evaluate cognitively, and remain inactive in decision-making.

These states are not sequential but coexist probabilistically.

The QS Cube formalizes this concept by representing the customer as a distribution across channel, engagement, and decision dimensions.

2.2. The Wave Function: Modeling Behavioral Uncertainty

This distribution can be conceptually described through a function:

ψ(s)

where s represents the possible behavioral states of the customer.

The square modulus:

|ψ(s)|2

represents the probability that the customer manifests a specific observable behavior (e.g., conversion, contact, purchase).

This formulation is not intended to introduce strict mathematical formalization, but to highlight a critical insight:

Customer behavior is inherently probabilistic, not deterministic.

2.3. Measurement

Measurement: Interaction as State Transformation

In quantum systems, the act of measurement does not simply reveal the state—it modifies the system itself.

A similar principle applies to customer interactions.

Every interaction—whether digital, human, or automated—acts as a measurement:

a marketing message

a chatbot interaction

a branch meeting

a product simulation

Each of these events not only reveals information about the customer, but alters the probability distribution of their future behavior.

2.4. Collapse

Collapse: The Emergence of Value

The most critical moment in the QS Cube is analogous to wave function collapse.

In physics, collapse occurs when a probabilistic system resolves into a single observable outcome.

In customer behavior, this moment corresponds to:

a decision

a subscription

a purchase

a commitment

At that instant:

uncertainty is resolved

probability becomes action

potential becomes value

Key Concept: Collapse as Value Creation

Value is not continuously generated.

It emerges discontinuously at the moment of decision.

This represents a central implication of the QS Cube.

Digital interactions increase probabilistic potential, while relational interactions accelerate the collapse into decision.

2.5. Non-Linearity and Path Dependence

Another key parallel with quantum systems is path dependency.

The sequence and nature of interactions shape outcomes in non-linear ways:

1) the same customer exposed to different stimuli produces different trajectories

2) small variations in interaction timing or context can lead to radically different outcomes

This explains why:

1) identical campaigns produce heterogeneous results

2) customers with similar profiles diverge behaviorally

2.6. From Observation to Orchestration

Traditional models observe behavior after it occurs.

The QS Cube enables something different: the ability to influence the probability distribution before the outcome emerges.

This implies a shift:

1) from classification → to probabilistic interpretation

2) from reaction → to orchestration

3) from channel management → to trajectory design

4. Discussion

From Quantum Behavior to Managerial Action

The value of the quantum perspective does not lie in its theoretical elegance alone. Its practical relevance emerges when these principles are translated into actionable frameworks.

If customer behavior is probabilistic rather than deterministic, then management cannot rely on static classification. It must shift toward continuous interpretation and active orchestration. This perspective is consistent with established frameworks in customer relationship management

.

The QS Cube is designed precisely for this transition.

It takes the core properties derived from the quantum analogy—superposition, measurement, and collapse—and translates them into a managerial model that can be used to guide decisions, allocate resources, and design customer journeys.

4.1. From Superposition to Customer Mapping

Superposition implies that customers exist in multiple states simultaneously.

Operationally, this means:

1) customers cannot be assigned to a single segment

2) behaviors must be represented as distributions across states

3) decisions must be based on probability, not classification

The QS Cube embodies this by mapping customers across three simultaneous dimensions:

Channel State → where interaction occurs

Engagement State → how strong the relationship is

Decision State → how close the customer is to acting

Instead of asking “Who is the customer?”, the model asks:

“Where is the customer in the probability space?”

4.2. From Measurement to Interaction Design

In quantum systems, measurement changes the state.

In customer systems, interaction does the same.

This has direct operational implications:

Every interaction is not just a touchpoint—it is an intervention.

This reframes how banks should design actions:

marketing is no longer communication → it is state transformation

service is no longer execution → it is probability adjustment

advisory is no longer support → it is trajectory acceleration

Within the QS Cube, each interaction is evaluated based on its ability to:

shift engagement upward

move the customer closer to decision

reduce uncertainty in a structured way

4.3. From Collapse to Value Strategy

The concept of collapse introduces a decisive shift in how value is managed.

If value emerges only at the moment of decision, then:

value is not distributed evenly across the journey

it is concentrated in specific states of the system

This leads to a fundamental principle:

Not all customer states are equally valuable.

The QS Cube allows organizations to identify:

low-value zones (exploratory, low engagement)

transition zones (activation phase)

high-value zones (decision-ready, high engagement)

The objective of management is therefore not to maximize interactions, but to:

orchestrate movement toward high-value states.

From Probability to Orchestration

Traditional models are reactive: they describe behavior after it occurs.

The QS Cube enables a different logic:

the proactive shaping of customer trajectories.

This transforms the role of the organization:

from observer → to orchestrator

from analyzer → to system designer

from channel manager → to trajectory manager

AI plays a critical role in this shift:

identifying probabilistic signals

predicting state transitions

triggering next-best actions

Human interaction remains central:

resolving uncertainty

building trust

enabling the final collapse into value

The role of artificial intelligence in enhancing decision-making and marketing effectiveness has been widely explored in prior research

| [12] | Payne, A., & Frow, P. (2005). A Strategic Framework for Customer Relationship Management. Journal of Marketing, 69(4), 167-176. https://doi.org/10.1509/jmkg.2005.69.4.167 |

| [13] | Porter, M. E., & Heppelmann, J. E. (2015). How Smart, Connected Products Are Transforming Companies. Harvard Business Review. |

[12, 13]

.

Operational Principle

Managing customers therefore entails managing probabilistic dynamics.

Value creation thus corresponds to enabling the collapse into observable decisions.

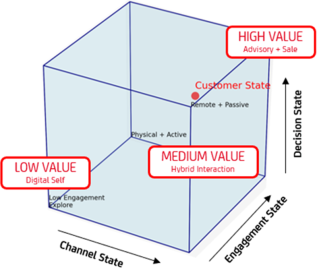

The QS Cube Framework

The QS Cube translates this into a managerial model across three dimensions:

Channel State (X)

How the customer accesses the system: digital, physical, remote

Engagement State (Y)

The intensity of the relationship: passive, active, latent

Decision State (Z)

The proximity to decision: explore, evaluate, decide

Customers are not points.

They are trajectories evolving in a probability space.

The QS Cube can be visualized as a three-dimensional probabilistic space in which customer behavior evolves across channel, engagement, and decision dimensions (see

Figure 1).

Figure 1. QS Cube framework.

Value Is a Trajectory, Not a Property

Traditional banking assigns value to segments or channels. The QS Cube challenges this: Value is not attached to who the customer is. It emerges from where the customer is going.

The highest value is generated when:

1) engagement is high

2) decision proximity is high

Three Phases of Customer Superposition

Phase 1 - Exploratory Superposition

1) digital-first behavior

2) low engagement

3) high uncertainty

high volume, low value

Phase 2 - Activation

1) increasing interactions

2) signals emerge

3) uncertainty decreases

AI plays a critical role

Phase 3 - Collapse

1) decision moment

2) probability becomes value

economic impact generated

A Customer in Superposition: A Practical Illustration

Consider Marco, a retail banking customer in his mid-40s.

Over several weeks, Marco repeatedly accesses the bank’s mobile app. He simulates mortgage options, compares scenarios, and explores alternatives. His behavior is intense—but entirely digital.

At this stage, he exists in an exploratory superposition: high activity, low engagement, distant from decision.

The system detects a pattern: repeated simulations, increasing frequency, growing coherence of intent.

A trigger is activated.

Marco receives a proactive invitation to meet a financial advisor. He accepts.

During the meeting, something changes. His needs become clearer. Uncertainty reduces. Options crystallize.

In QS Cube terms, his state shifts:

1) from digital - passive - explore

2) to assisted - active - evaluate

Then comes the moment.

Marco decides. He subscribes to a mortgage product.

The Moment of Value

This represents the collapse of the probabilistic state. What was probability becomes a concrete decision. What was potential becomes value.

Value is not generated by the channel itself, but by the trajectory.

The Branch as a Value Engine

The branch does not execute transactions—it transforms probability into decisions.

In the new paradigm, the branch is no longer an operational site. It becomes the point where customer trajectories converge and resolve. It is not simply one channel among many, but a discontinuity point—where uncertainty is converted into commitment.

Within the QS Cube, this moment corresponds to the collapse of the probabilistic distribution: the transition from multiple possible states to a single observable outcome. Opening an account, making an investment, committing to a financial decision—these are all manifestations of that collapse.

Value is not distributed evenly along the journey, nor is it embedded in the customer or the channel itself.

It emerges precisely at that moment.

Value does not exist before the decision. It is created in the interaction that makes the decision possible.

In this sense, the branch evolves from a point of execution into a value-creation environment, where relational interaction becomes the critical mechanism for converting potential into economic outcomes.

AI and Strategic Transformation

Artificial intelligence does not eliminate human value—it unlocks the capacity to create it at scale.

AI is often framed as a force of substitution, reducing the need for human labor through automation and efficiency gains. Within this narrative, increased productivity is typically associated with workforce reduction.

The QS Cube suggests a fundamentally different interpretation.

AI does not merely eliminate tasks.

It reallocates where value can be created.

By automating repetitive and transactional activities, AI dramatically improves productivity. Tasks that once absorbed time and resources—processing, execution, routine interactions—are increasingly handled by intelligent systems.

This creates a structural effect: excess human capacity.

In traditional models, this surplus is treated as inefficiency to be eliminated.

Within the QS Cube, it becomes the primary opportunity for value creation.

From Operational Efficiency to Value Expansion

Freed from operational constraints, human resources are no longer bound to execution. They can be redirected toward activities that matter most within a probabilistic system:

reducing customer uncertainty

strengthening engagement

enabling decision-making

In other words: productivity gains generated by AI are converted into advisory capacity.

This represents a critical shift.

The organization does not necessarily become smaller.

It becomes more capable of generating value per interaction.

How AI Transforms Value Creation in the QS Cube

From efficiency gains to value expansion

Step 1 — Automation Creates Capacity

AI automates repetitive and transactional activities:

1) processing

2) execution

3) routine interactions

Productivity increases

Operational workload decreases

Step 2 — Capacity Becomes Opportunity

The organization faces a structural shift:

An excess of human capacity emerges.

Traditional response:

1) reduce workforce

QS Cube perspective:

2) redeploy capacity toward value creation

Step 3 — Human Work Shifts to Value Creation

Freed resources move toward:

1) advisory interactions

2) relationship building

3) uncertainty reduction

4) decision enablement

From tasks → to impact

From execution → to influence

Outcome: The New Operating Model

1) AI handles probability at scale

2) humans act where decisions happen

3) the branch becomes a consultative hub

Strategic Shift

Table 1. QS Cube Model.

Traditional Model | QS Cube Model |

Efficiency → cost reduction | Efficiency → value expansion |

Workforce reduction | Capacity redeployment |

Channel execution | Trajectory orchestration |

Transactions | Decisions |

Core Insight

The real impact of AI is not fewer people.

It is more value created by the same people.

The Reinvention of the Branch

As this transformation unfolds, the role of the branch evolves accordingly.

No longer a processing center, the branch becomes a consultative environment where human interaction is deployed precisely when it has the highest impact on customer trajectories.

Operational redundancy is not a loss—it is a resource reallocation mechanism.

Employees previously engaged in transactional activities are repositioned into advisory roles, where their contribution directly influences the likelihood of decision.

Excess capacity created by AI is not waste. It is unexpressed value waiting to be activated.

AI, Humans, and the Moment of Collapse

AI excels at:

detecting probabilistic signals

predicting behavioral trajectories

triggering next-best actions

But it does not create value by itself.

Value emerges at the moment of decision—the collapse

| [15] | Kumar, V., & Reinartz, W. (2016). Creating Enduring Customer Value. Journal of Marketing, 80(6), 36-68

https://doi.org/10.1509/jm.15.0414 |

| [18] | Busemeyer, J. R., & Bruza, P. D. (2012). Quantum Models of Cognition and Decision. Cambridge University Press. |

[15, 18]

.

And that moment is still fundamentally human.

trust is built in interaction

uncertainty is resolved through dialogue

commitment is enabled relationally

AI manages probability at scale.

Humans transform that probability into value.

Strategic Principle

The goal is not to simplify the customer. The goal is to orchestrate complexity.

6. Recommendations

Translating the QS Cube into operational impact requires moving from observation to active orchestration of customer trajectories. Organizations can implement the framework through five concrete steps.

6.1. Map Customers as Probability Distributions

Replace static segmentation with probabilistic mapping.

Represent customers across channel, engagement, and decision dimensions

Identify where customers are likely to evolve next

The assignment of customers to fixed categories should be avoided

The goal is not classification, but dynamic positioning within the QS Cube.

6.2. Identify High-Value States

Not all customer states generate value.

Low-value zone: digital exploration, low engagement

Transition zone: activation and signal emergence

High-value zone: strong engagement, decision proximity

Value is concentrated in moments of decision, not evenly distributed.

6.3. Design Interactions as State Interventions

Every interaction must be treated as a transformation mechanism.

Digital channels → increase probability

Advisory interactions → accelerate decision

AI triggers → reduce uncertainty

Each touchpoint should be evaluated based on its ability to move the customer toward higher-value states.

6.4. Orchestrate Trajectories, Not Channels

Move from channel management to trajectory management.

coordinate digital and physical touchpoints

use AI to anticipate behavioral transitions

activate human interaction at critical decision moments

The objective is not omnichannel presence, but controlled movement across states.

6.5. Optimize the Moment of Collapse

Organizational focus should be directed toward decision points.

1) strengthen advisory capabilities

2) ensure availability at critical moments

3) remove friction in decision processes

Value is created when probability collapses into action.

Managerial Takeaway

The QS Cube does not claim that customers behave as quantum particles. Rather, it adopts the mathematical and conceptual structure of quantum theory as the most coherent way to represent uncertainty, coexistence of states, and decision emergence in complex behavioral systems.

Winning organizations do not manage customers.

They manage probability and orchestrate its conversion into value.