Abstract

Objective of this manuscript is both to tracing the evolution of money, and examining its transition from commodity money to fiat money, up to the emergence of cryptocurrencies. It highlights the inherent issues of the barter system, emphasizing the urgencies and necessities that favored the adoption of legal tender. Subsequently, the impact of the creation of the Euro on the European economy—both historically and geopolitically—will be analyzed, contextualizing the European Union's institutional process. In a response to the crisis, Bitcoin (the first decentralized cryptocurrency) will be introduced, along with an illustration of the supporting Blockchain technology will be provided. Finally, the proposal of American Senator Lummis, who suggests a massive purchase of Bitcoin to be used as a strategic reserve through the “Bitcoin Act” program, will be explored, prompting several reflections on the future of the petrodollar as a reserve instrument. Through these reflections, the reader could develop their own thoughts on the importance of evolving towards forms of money more suited to an increasingly digitized and decentralized economy. In conclusion, by proposing an analogy between the ancient monetary practices on Yap and cryptocurrencies, we aim to stimulate the reflection that innovation is not only desirable in this fast-paced world but essential.

Keywords

Monetary Evolution, Cryptocurrency, Decentralization, History, Money Value, Finance

1. Introduction

When we want to define people as wealthy, we often say they have a lot of money. For a more specialized discussion, we will use the term "money" instead of "cash," identifying the former as a specific type of wealth, particularly as a reserve of readily available values to facilitate transactions

| [26] | Mankiw, N. G., & Taylor, M. (2011). Macroeconomia. Quinta edizione italiana aggiornata alla settimana edizione americana. |

[26]

. Generally, money is needed for three primary functions: as a unit of account, as a store of value, and most importantly, as a medium of exchange.

When referring to a store of value, we mean the instrument that transfers purchasing power from the present to the future. For instance, an individual who holds a certain amount of money can decide to retain it to spend tomorrow, next week, next month, and so on. Naturally, it will be exposed to inflation risk, where rising prices erode their purchasing power of money. Therefore, it can be defined as an imperfect store of value

| [29] | Msefula, G., Hou, T., & Lemesi, T. (2024). Financial and market risks of bitcoin adoption as legal tender. Evidence from El Salvador (Vol. 11(1)). Humanities and Social Sciences Communications. https://doi.org/10.1057/s41599-024-03908-3 |

[29]

.

As a unit of accounts, money represents the measurement method through which economic transactions are quantified

| [22] | Levant, Y., & Nikitin, M. (2020). History of an unsuccessful performance measurement innovation: surplus accounts in France (1966–c.1990). Accounting History Review, 30(3), 307-339. https://doi.org/10.1080/21552851.2020.1810722 |

[22]

. It also allows for the setting of prices for buying and selling. For example, a merchant lists the price of goods in current currency, while a creditor is entitled, in due times, to ask the debtor for a certain amount of money in exchange for a certain quantity of any good.

Thus, money is the primary tool for exchanging goods and services and is correlated with another important property called liquidity, the speed at which money can be converted into services and tangible or intangible goods. However, in order to better understand the functions of money, a step back to the early Middle Ages is necessary. This was the era of early domestic communities, organized around simple and socially shared rules. It was the era of the so-called subsistence economy, where hunting or harvesting practices were meant to satisfy primary needs (such as the sustenance of family members), with the remainder exchanged within the community. This was the time of barter-based economic systems, where exchanges required the unlikely circumstance of a double coincidence of needs—everyone must desire what the other has, at the same place and time. To illustrate the limitations inherent in a barter-based economy (where only modest transactions can occur), it is apt to refer to Adam Smith's thoughts, who, while investigating the limitations of the ancient barter technique, wrote:

"Suppose a man has more of a certain commodity than he needs while another has less. Consequently, the first would be happy to dispose of the surplus and the second to buy it. But if the second has nothing that the first needs, no exchange can take place between them

| [4] | A. Smith. (1973). Indagine sulla natura e le cause della ricchezza delle nazioni. Arnoldo Mondadori Editore. |

[4]

. And further: "One who wanted to buy salt but had only cattle to exchange would have been forced to buy salt to the value of an entire ox or sheep at once. He could hardly buy less, as what he had to trade could not be divided without loss

| [4] | A. Smith. (1973). Indagine sulla natura e le cause della ricchezza delle nazioni. Arnoldo Mondadori Editore. |

[4]

.

Thanks to Smith, we can understand the urgent demands of barter, namely that the diverse exchange needs often not only coincide but are also perfectly compatible with the actual availability of goods to be exchanged

. Essentially, the person desiring a good had to find an individual who was not only willing to trade it but also interested in what was offered in return. An additional critical issue concerned indivisible goods, especially animals: those who owned an animal had to find someone with a quantity of goods equivalent in value to the whole animal to engage in barter

.

The transition from national currencies to the Euro marked a significant shift in monetary policy, fostering economic integration within the European Union. However, global financial crises, particularly the 2008 Great Recession, exposed vulnerabilities in traditional banking and monetary systems, leading to increased public interest in decentralized alternatives. The emergence of Bitcoin, initially perceived as a response to the instability of centralized financial institutions, represents a paradigm shift in how money is conceptualized and transacted. Despite its growing adoption, cryptocurrencies still face considerable skepticism due to the lack of regulatory frameworks, which fosters distrust among governments, financial institutions, and the general public. The absence of clear regulations raises concerns about security, market volatility, and illicit financial activities. However, despite these challenges, the global financial system is undergoing profound changes driven by the rise of digital assets. The increasing acceptance of Bitcoin as both a means of exchange and a store of value, alongside discussions about its potential role in national reserves, signals a transformative period in monetary history.

In modern economies, where trade is indirect, and the complexity of transactions is high, it has been necessary to resort to a unique instrument, recognized by all parties involved as having the same value: money. In advanced economies, hundreds of thousands of transactions are executed daily with printed paper bills that function solely as money: these are banknotes, which would have no value in transactional operations if the parties involved did not recognize them as money. Indeed, money that has no intrinsic value (and banknotes, understood as colored pieces of paper, do not) is formally referred to as fiat money, from the Latin fiat, meaning order, as its value in the community is defined by legislative decree

| [18] | Friedman, M. (1960). A program for monetary stability. New York: Fordham University Press. |

[18].

Although its use in advanced economic systems is considered the norm, over the centuries, goods with intrinsic value have often been used to regulate exchanges: this type of money is known as commodity money, with the most notable and widespread example being gold.

Before delving into the gold standard, it is interesting to mention an episode during World War II in European prisoner-of-war camps: the Red Cross supplied the prisoners with various comfort items, from food to clothing, and even cigarettes. The distribution methods did not account for the personal needs (and preferences) of each prisoner, often resulting in inefficiency (one might prefer cheese over chocolate, another might need a shirt, and so on). Therefore, prisoners began bartering goods among themselves. Soon, due to the limitations of the resource allocation system of barter (remember, the double coincidence of wants), even in an economy as limited as that of a prisoner-of-war camp, it became urgent to find and resort to a monetary instrument to simplify transactions. Thus, cigarettes became a store of value, a unit of account, and a medium of exchange; they became the currency in which "prices" were expressed and transactions between prisoners were regulated: for example, a shirt "cost" eighty cigarettes, while laundry services "cost" two cigarettes per garment. In such an economic system, even non-smokers began accepting cigarettes as payment, aware that they could exchange them in the future for other goods they might need

| [33] | Razavi, R., & Elbahnasawy, N. (2025). Unlocking credit access: Using non-CDR mobile data to enhance credit scoring for financial inclusion. Finance Research Letters, Vol. 73(106682). https://doi.org/10.1016/j.frl.2024.106682 |

[33]

.

These are examples of goods that served as commodity money until the end of the 19th century: the Mexican cacao market, the almond trade in Surat, India, salt and hides in Ceylon (Sri Lanka), Nigerian peanuts, stones on the island of Yap

, tea bricks in Tibet and southern Siberia, cowries (shells resembling porcelain) in tropical countries, bird feathers in the New Hebrides archipelago, and textiles in Japan, China, and West Africa

| [40] | Weineer, A. B. (1992). The meaning of Money: The role of Money in the Economy. University of Hawai. |

[40]

.

Tracing back to the era of gold, it is no surprise that individuals throughout history have been willing to accept it as a payment instrument; gold is an exhaustible metal (which gives it high intrinsic value), it shines, is very malleable, and its purity is relatively easy to assess (one could simply heat it in a pot over a fire to melt it, let it cool, and check that, after this intense thermodynamic cycle, the metal still shines).

A spontaneous question arises: why, given the possibility of conducting transactions in gold, has something without intrinsic value, such as fiat money, been used instead?

To answer this question, imagine an economy where its participants are forced to carry sacks filled with gold bars to conduct exchanges. On one side, the buyer would need to measure the appropriate amount of gold to give. On the other side, the seller, besides agreeing with the buyer on its weight, would have to verify the metal’s purity. If each commercial transaction required lighting a cauldron, one can understand the burden—broadly speaking—of the transaction itself, especially in terms of time.

Moreover, gold has a high density, and thus a weight that makes it inconvenient to move, considering the high risk of it being extorted from the holder during transport. To reduce all costs generated by transactions in these monetary systems, the State initially intervened by minting gold coins, guaranteeing their weight and purity, thus recognizing equal value among all economic operators. The State collected gold from savers in exchange for gold certificates, i.e., paper notes of the same value as the precious metal, convertible into a predetermined and certain quantity of gold upon the holder’s request.

Lighter than both gold bars and gold coins, paper notes simplified transactions, being easily transportable, and became the monetary standard precisely because of the State’s guarantee to convert them upon request. Thus, if in every transaction, the buyer uses the paper note and the seller accepts it as payment (recognizing its value), a system based on commodity money naturally evolves into a system with fiat money

. However, note that the use of money in transactions is a true form of social convention, in the sense that each individual assigns value to fiat money simply because they hold the reasonable expectation that everyone will use the same method.

2. Methodology

This study employs a multidisciplinary and qualitative research approach to examine the historical, economic, and technological evolution of money, tracing its development from the barter system to fiat currency and, ultimately, to decentralized digital assets such as Bitcoin. Given the complex nature of monetary systems and their socioeconomic implications, this research integrates historical analysis, economic theory, and comparative case study methodology to provide a comprehensive understanding of financial transformation over time.

To achieve this, the study systematically reviews primary and secondary sources, including classical economic theories, institutional reports, policy documents, and legislative frameworks. A historical perspective is adopted to investigate the intrinsic limitations of the barter system, the necessity for legal tender, and the subsequent adoption of fiat money. Additionally, the research explores the implications of the creation of the Euro within the European Monetary Union (EMU), considering both its geopolitical and economic ramifications. Through a structured examination of institutional processes and monetary policies, the study contextualizes the role of central banks and governmental interventions in shaping modern financial landscapes.

A key aspect of the methodology involves comparative analysis, where historical monetary systems are juxtaposed with contemporary financial innovations. In particular, the study draws analogies between the ancient Yapese monetary system—where large stone discs served as a store of value and unit of exchange—and the decentralized nature of cryptocurrencies. This comparative framework enables a deeper understanding of how historical precedents inform the conceptual foundations of Bitcoin and blockchain technology, particularly in terms of trust, decentralization, and the absence of physical transfer in monetary transactions.

Furthermore, the study incorporates a geopolitical and financial stability lens to assess the broader macroeconomic consequences of digital currencies. By analyzing the adoption of Bitcoin as a reserve asset, particularly in the context of proposals such as the Bitcoin Act in the United States, the research evaluates potential shifts in global monetary power and the future of reserve currencies. The methodological approach also considers the economic implications of cryptocurrency adoption, including its impact on inflation, monetary sovereignty, and financial inclusion.

To ensure a rigorous and balanced analysis, the study synthesizes insights from academic literature, policy papers, and empirical data where available. While qualitative in nature, the research remains anchored in theoretical frameworks from monetary economics, financial history, and political economy, enabling a holistic assessment of the transition from centralized to decentralized financial models. The study’s interdisciplinary approach not only provides a historical foundation but also offers forward-looking reflections on the role of digital assets in an increasingly digitized and interconnected global economy.

3. Founding of the European Union and Process of Change

In the period between the late 1990s and 2000, some countries decided to abandon their respective currencies (which had served as legal tender for hundreds, if not a thousand, years) to adopt a new and common currency, the euro, thus establishing the European Economic and Monetary Union (EMU). To provide a more textbook definition, a monetary union (or currency union or currency area) is the group of countries that have adopted the same currency as a means of exchange and have permanently and irrevocably adopted a regime of fixed exchange rates between their respective currencies. The currency area of the countries that have adopted the euro is known as the EMU, and the member nations are included in the eurozone or euro area

| [26] | Mankiw, N. G., & Taylor, M. (2011). Macroeconomia. Quinta edizione italiana aggiornata alla settimana edizione americana. |

[26]

. Since adopting the euro, the EMU countries have agreed to share the same monetary policy, arranged and implemented by the European Central Bank (ECB) in agreement with the central banks of each member state, forming the European System of Central Banks (ESCB).

When discussing Europe and the European Union (EU), one is identifying a specific physical portion of the continent and the collective twenty-seven member states in a political and economic organization with supranational characteristics, authorized to make decisions in certain areas (such as economic and monetary policy) that hold greater weight than the actions and will of the individual member territories.

The process of establishing the current EU has been long and finds its roots in the aftermath of World War II. Starting from the 1950s, the global conflict had just ended, and the Nazi German attempt to dominate the continent had been thwarted. The global geopolitical landscape saw a contrast between Europe and the United States on one side and the Soviet Union on the other, with differing political, economic, and social visions. Stanciu and Partsch

argue that political beliefs and social dynamics significantly influence cryptocurrency adoption, reinforcing the societal shifts Bitcoin represents.

The United States, fearing that Western Europe might succumb to Soviet influence or even hegemony (which would create a new superpower difficult to counter) and that Germany might rearm, decided to encourage and support the progressive unification of European countries under a single banner.

On April 18

th, 1951, the embryo of the EU took shape: the Treaty establishing the European Coal and Steel Community (ECSC) was signed in Paris (entering into force on July 23

rd, 1952), with Italy

, France, the Netherlands, Belgium, Luxembourg, and the Federal Republic of Germany (or West Germany, as East Germany was under Soviet control) aiming at creating a single market for these two significant raw materials

. These two materials were particularly significant because, at the time, coal was the primary energy source, and steel was crucial not only to produce machinery but also for weaponry. With the ECSC, the economic core of Europe began to unite, and the outcomes could only be favorable in the eyes of the United States: on one hand, Germany's autonomy concerning the two raw materials (steel even more so than coal for rearmament) was weakened; on the other hand, by economically uniting, some of the main European states formed a block of interest strong enough to sustain itself, distancing itself from the Soviet Union. In short, the EU laid its foundations on purely geopolitical matters: it was born, largely but not entirely, from the initiative of an actor external to Europe (the USA) to curb the expansion of another external actor (the Soviet Union) and to restrain a European country (Germany). In this vein, Chey

frames cryptocurrencies within the International Political Economy, shedding light on their potential to disrupt traditional monetary hierarchies and geopolitical strategies

.

Moving forward, on March 25

th, 1957, the same six founding countries of the ECSC signed the Treaty of Rome (which would come into force on January 1

st of the following year), establishing the European Economic Community (EEC) to stimulate the economic growth of its members (not limited to the production and trade of coal and steel) and increase trade through the progressive abolition of customs duties, or the passage taxes between countries

. The declared long-term goal of the EEC was to create a common European market characterized by the free movement of people, goods, services, and capital; a goal significantly boosted in 1986 with the signing of the Single European Act (SEA) in Luxembourg on February 17

th and in the Netherlands on February 28

th.

Returning to the historical narrative, from the 1970s (initially as the EEC, then as the EU) the union attracted and welcomed other states beyond the six founders. The first was the United Kingdom (which later withdrew with Brexit), followed by Ireland and Denmark in the same year; subsequently joined by Greece (1981), Portugal and Spain (1986), Austria, Finland, and Sweden (1995), Czech Republic, Cyprus, Estonia, Latvia, Lithuania, Malta, Poland, Slovakia, and Hungary (2004), Bulgaria and Romania (2007), Croatia (2013).

On February 7

th, 1992, the Treaty on European Union was signed in Maastricht (Netherlands)

.

With its entry into force on November 1, 1993, the term European Economic Community changed to European Community (EC) with a well-defined aim and a bold aspiration: to merge the member states not only in economic aspects but also politically and monetarily, while laying the groundwork for structuring the United States of Europe (a goal that today seems far from achievable). The Maastricht Treaty also defined the criteria (convergence criteria) for admission to the euro area, setting stringent requirements:

1. Strict limits on the annual state budget deficit, prohibiting it from exceeding 3% of the Gross Domestic Product (GDP);

2. Prohibition of public debt exceeding sixty percent of GDP;

3. Inflation rate containment within one and a half percentage points of the average inflation rate;

4. Prohibition of exceeding the average inflation rate of the three countries with the lowest inflation by two percentage points.

Following further institutional steps, with the Lisbon Treaty, in effect from December 1

st, 2009, after ratification by all member states, the European Union assumed its current structure

.

In the monetary field, since January 1st, 2002, the euro has replaced the national currencies of 19 out of 27 EU countries, although it was introduced three years earlier and its use was limited to electronic circulation through information systems for accounting purposes and electronic payments, thus serving as virtual money. Crucial to the euro's replacement of national currencies was the determination of the exchange rate, i.e., determining the value of individual European currencies against the euro once converted. The conversion rates were established by the European Council based on EU recommendations and market rate assessments in December 1998. The euro currency symbol is inspired by the Greek letter epsilon, as a tribute to Greece, the cradle of European and Western civilization. The monuments depicted on banknotes are imaginary creations: the bridges and arches symbolize the union between member countries, and the decision to avoid depicting real structures was carefully considered to prevent favoritism and nationalism. Since 2013, a redesign of the euro has been underway to give it a new graphic design and enhance its security features.

4. The Crisis the World Cannot Recover from the Great Recession of 2008

The rules of the global economy were entirely rewritten by an event that, in 2008, marked the socio-economic policy worldwide: the Great Recession

. To trace the origins of the 2008 crisis—which may seem strange—one must start with a basic human desire of owning a home

| [19] | Gorton, G. (2010). Slapped by the Invisible Hand: The panic of 2007 (Financial Management Association Survey and Synthesis ed.). Oxford University Press. |

[19]

. To purchase a property, individuals often take out a mortgage. However, this financial operation is not accessible to everyone, as one must approach a credit institution that, based on an analysis of the potential debtor's financial behaviors, will issue an evaluation determining the individual's reliability in accessing the loan. This evaluation is better known as a credit score. Thus, to buy a house, one must take out a mortgage (if the necessary amount is not held), and to obtain a mortgage, one needs a good credit score. The potential debtor must demonstrate having stable employment and sufficient income to meet payment deadlines, not being excessively indebted, and having a credit history showing they have previously been able to meet installment payments regularly. Additionally, it is necessary to guarantee the credit institution that someone or something can settle the debt in case of debtor default. In the case of a mortgage, the guarantee is the house itself, meaning if the debtor fails to meet payments the bank acquires ownership of the property. Given this, the difficulties of taking out a mortgage become evident. However, in 2004, in the United States, the doors of paradise opened, so to speak: The Federal Reserve Bank took drastic measures to restart the economy, even cutting interest rates, which, if they hovered around 6.5% in the early 2000s, dropped to around 1%. This situation led to a steady increase in mortgage requests. In response, banks—seeing potential significant profits from such credit issuance—began drastically lowering their credit score requirements and granting so-called subprime mortgages to individuals who, under pre-2004 conditions, would not have qualified

| [24] | Lim, K., Liu, C., & Zhang, S. (2024). Optimal central banking policies: Envisioning the post-digital yuan economy with loan prime rate-setting. Emerging Markets Review, Vol. 59(101108). https://doi.org/10.1016/j.ememar.2024.101108 |

[24]

. To protect themselves from debtor default risk, banks inserted a clause in mortgage contracts stipulating that the fixed interest rate would change to variable at a predetermined time: the mortgage would start with a fixed rate, allowing even less affluent citizens to meet payments, and then follow market rates at a later stage. If the central bank decided to raise interest rates, the rates for commercial banks would also rise. Consequently, variable mortgage rates would increase, and individuals initially solvent at the time of contract signing would become insolvent and unable to meet payment obligations. The debtor has two options: refinance the mortgage, incurring more debt, or face foreclosure

| [34] | Roubini, N., & Mihm, S. (2010). Crisis Economics: a crash course in the future of finance. New York: Penguin Books. |

[34]

.

American banks aimed at operating in a win-win scenario. Indeed, if the debtor paid the mortgage installments, they received liquidity, while if the debtor defaulted, the property would be foreclosed, and ownership would transfer to the bank, which could then market the property. By 2004, the real estate market had soared, with house prices on an upward trend, making investment profitable. Major investors, particularly banks, decided to go all-in: the more mortgages issued, the more liquidity returned as passive interest.

To grant such extensive credit, it was necessary to scale up credit score assessments. Concurrently, precise credit score evaluations slowed mortgage issuance processes. Consequently, credit score controls were relaxed, leading to so-called ninja loans (No Income, No Job or Asset). In this context, the real estate market generated eleven million new mortgages in 2005 alone, which appeared as a very secure investment to banks. On the other hand, everyone felt the tangible possibility of purchasing a home, if not more than one

| [6] | Ballester, L., González-Urteaga, A., & Shen, L. (n.d.). Green bond issuance and credit risk: International evidence. Journal of International Financial Markets, Institutions and Money, Volume 94(102013). https://doi.org/10.1016/j.intfin.2024.102013 |

[6]

.

The issuance of so many mortgages results in the banks holding a substantial package of credits. These are grouped (or rather, securitized) into credit securities, the most well-known of which are the so-called CDOs (Collateralized Debt Obligations). The credit institution issues numerous mortgages, bundles its credits into CDOs, and sells them on the market, including Wall Street and banks in many countries worldwide, including Europe. By doing so, the bank (by selling the credits on the market) relinquishes the installments due from debtors but, in return, can generate liquidity that can immediately be used to grant further mortgages, package the credits into additional CDOs, and sell them on the market. Thus, there is a vicious cycle fueled by the growth of the real estate sector, which, in turn, is fueled by the excessive granting of credit.

CDOs have never been more heterogeneous, composed of various types of mortgages, from prime, with low default risk, to subprime, with higher risk. Consequently, there is a need to assign a rating to the credit packages indicating the quality of the different tranches of CDOs: if these contain many subprime mortgages, the default risk is high, and one would expect the rating assigned by agencies (Fitch, Moody’s, Standard & Poor’s) to be low. However, if they contain more prime mortgages, the default risk is significantly lower, and a higher rating is expected. However, the reality is quite different. Since the evaluation by rating agencies is fundamental for selling the CDOs, the assessment of various tranches of credit packages is often erroneous and inflated, with tranches receiving AAA ratings (indicating the highest solvency and representing a guarantee for potential buyers) despite containing subprime mortgages.

What is the reason behind such high ratings assigned to packages containing subprime mortgages? The truth is that, on one hand, evaluating CDOs was arduous as they were bundled into new CDOs (containing a diverse quantity of credits, complicating any risk analysis) sold to investment banks. On the other hand, rating agencies—competing fiercely—had a vested interest in not losing clients, and the easiest way to retain banks was to assign favorable ratings to their CDOs.

Now, consider the perspective of a commercial bank: holding AAA-rated CDO packages, it can sell them to investment banks at a high price (due to the high rating) and record the proceeds as revenue. Whether the mortgage contracts within the packages are settled or not is no longer a concern, as selling the CDOs has transferred ownership of the credits and, crucially, the default risk to the buyer. The buyer, in turn, purchases a package of credits rated at minimum default risk by accredited and reputable agencies. This market satisfies everyone, but the risk looms large.

In 2004, Federal Reserve Bank (Fed) began raising interest rates to curb economic expansion, which was advancing rapidly and causing inflation issues. The U.S. economy was booming, and consistent with supply and demand theories, prices began to rise; however, the cost of living increased without a corresponding rise in wages.

As previously mentioned, when the Fed raises interest rates, commercial banks also raise rates for debtors: if mid-2004 Fed rates were 1%, by the end of the year, they rose to 2.25%, and a year later to 4%. Despite this, no changes in the mortgage market were observed, and for many individuals, homeownership remained their only asset.

However, the moment arrives when variable rates on existing mortgages are triggered. On average, those who took out subprime mortgages found themselves facing a 30% increase in installments compared to the original mortgage contract by the end of 2007. As mentioned earlier, the cost of living had risen, but wages had not. The first difficulties in settling mortgage payments and subsequent foreclosures began. The property of homes used as credit collateral was transferred to the lending banks, which hoped to sell them in the real estate market and recover liquidity. This circuit could only be sustained if there were buyers. However, the same clients who previously fueled the system could no longer afford mortgage payments, letting alone purchase property.

From 2004 to 2007, over four million American families faced home confiscation. This figure could not be ignored: investment banks began buying fewer CDOs from commercial banks, which subsequently faced severe losses, unable to generate liquidity from CDO sales, insolvent debtors, or the sale of foreclosed properties. The house of cards collapsed: on September 15th, 2008, financial giant Lehman Brothers declared bankruptcy, with debts exceeding six hundred billion dollars. Simultaneously, the Dow Jones closed with its worst drop since September 11th, 2001, losing five hundred points. Between 2008 and 2009, eight million people in the United States lost their jobs, and over six million lost their homes. This crisis resulted from Wall Street's greed, the lack of financial education that led debtors to sign subprime mortgage contracts (which subsequently bankrupted them), and the unethical behavior of those who issued those mortgages.

It is the worst crisis since 1929, and the tragedy is that it would ripple across the entire world, as CDOs and other securitized packages were scattered among banks globally. The crisis quickly hit Europe: in 2009, the Eurozone Gross Domestic Product (GDP) dropped by 4.5%, unemployment rose to 10% (peaking at 20% in Spain), and global trade contracted by 12%. It is a complete economic halt.

5. Blockchain and Bitcoin

In the late 1980s, a group of activists known as Cypherpunk began to emerge on the Internet. Its members communicated through encrypted and anonymous mailing lists, aiming at utilizing cryptography to create and to disseminate information systems accessible to all people, by at the same time ensuring their privacy.

On October 31

st, 2008, about forty days after the collapse of Lehman Brothers—a symbol of the 2008 Great Recession—an individual named Satoshi Nakamoto sent a detailed proposal for a new peer-to-peer electronic money system to a Cypherpunk activist mailing list. The proposal included a nine-page PDF file, now commonly known as the Bitcoin "white paper"

. Among the few respondents was Hal Finney, who showed such interest in the project that, no later than two months later, on January 12

th, 2009, he received ten Bitcoins from Satoshi. This marked the second Bitcoin transaction (the first occurred nine days earlier), and it was the day Satoshi realized the system truly worked. It continued to function due to its "trustless" nature, meaning that its members did not need to know or trust each other for it to operate effectively.

While the identity of Satoshi Nakamoto remains shrouded in mystery after all these years (some believe he is a group of expert programmers and economists), it is undeniable that he created the cryptocurrency known as Bitcoin.

A cryptocurrency is a medium of exchange, like the euro or the dollar, but it exists solely in digital form as data exchanged between computers. While traditional currencies are issued by governments or central banks (the euro by the ECB, the dollar by the Fed), Bitcoins are created by an algorithm (also created by Satoshi) that not only generates the currency but also manages transactions involving it without the need for institutional intermediaries, making the transaction completely decentralized.

Bitcoins are exchanged using an innovative technology known as Blockchain, which can be simplistically understood as an encrypted digital ledger shared among all its users, where all Bitcoin transactions are recorded starting from the first on January 3

rd, 2009

| [5] | Angell, N. (1929). The Story of Money. New York: Frederick A. Stokes Company. |

[5]

. Blockchain technology was devised in 1991 by two American researchers, Stuart Haber and Scott Stornetta, intended to timestamp digital documents so they could not be backdated or tampered with

. However, the technology remained unused until 2008, when it became the cradle of the first cryptocurrency, Bitcoin.

A Blockchain is literally a chain of blocks containing information; each block contains three elements:

1. The stored data: The type of data depends on the Blockchain; Bitcoin's Blockchain stores details about the sender, receiver, and amount of cryptocurrency exchanged.

2. The hash: A string of numbers and letters uniquely identifying the block and its contents, like a fingerprint. Whenever a new block is created, a new specific hash for that block is generated. If any data within the block changes, the hash changes as well

| [15] | Comandini, G. (2021). Da Zero alla Luna - Quando, come, perché la blockchain sta cambiando il mondo. II edizione ampliata, Pages 53-65. |

[15]

.

3. The previous block's hash: Essential for creating the chain and ensuring the Blockchain's security.

Consider an example: imagine a Bitcoin Blockchain chain with three blocks, each containing its hash and the previous block's hash (the first block, not referencing any previous block, is called the genesis block). Suppose the second block is tampered with: its hash would automatically change, and consequently, the following block would be invalid because it would no longer contain the valid hash of the previous block.

The hash system is effective, but modern digital devices computing power makes it insufficient alone to prevent tampering. Some computers can calculate hundreds of thousands of hashes per second, theoretically allowing them to tamper with a block and recalculate the hashes of all other blocks to revalidate the Blockchain. To prevent this, Blockchain employs a cryptographic protocol known as Proof of Work (PoW), which essentially requires additional calculations to slow down new block creation, making Blockchain hacking attempts complex. In Bitcoin's case, it takes ten minutes to calculate PoW and add a new block to the chain, making tampering arduous as recalculating PoW for all subsequent blocks would be necessary. This process would be time-consuming.

Another peculiarity of Blockchain is decentralization: instead of a centralized entity managing the chain, it uses a peer-to-peer network that anyone can join and participate in. Those who join become network nodes and receive a complete copy of the Blockchain, verifying that everything functions correctly. When a new block is created, it is sent to all network nodes, which verify it to ensure it has not been tampered with. If it passes verification, they add it to their Blockchain.

As Budish

argues, decentralized technologies like Blockchain address the economic challenges of building trust at scale, a critical response to the loss of confidence in traditional financial systems post-2008. Recent developments in cryptocurrency adoption highlight the increasing role of decentralized financial systems in addressing economic inequality and financial inclusion. Studies suggest that cryptocurrencies could empower underbanked populations by providing access to digital payment systems and credit mechanisms

| [14] | Cicchiello, A. F., Cotugno, M., Monferrà, S., & Perdichizzi, S. (2022). Which are the factors influencing green bonds issuance? Evidence from the European bonds market. Finance Research Letters, Volume 50(103190). https://doi.org/10.1016/j.frl.2022.103190 |

[14]

. Furthermore, the potential of stable coins to mitigate currency volatility in developing economies underlines their transformative capacity. Integrating such innovations within the broader discourse on monetary evolution aligns with Bitcoin's trajectory, reinforcing its dual role as both an alternative financial instrument and a catalyst for economic restructuring. This progression reflects societal demands for transparency, efficiency, and inclusivity in financial systems.

If a node adds a tampered block, it will be rejected by all other network nodes. Today, Blockchains are primarily used to record cryptocurrency transactions, but they are also well-suited for securely storing any type of data, from digital contracts (smart contracts) to medical records and even creating signed digital artworks (Non-Fungible Tokens).

The Bitcoin Blockchain is entirely free, meaning the algorithm that makes it functional is public domain, not patented or owned by anyone. Additionally, the Bitcoin Blockchain's ledger is transparent, making information regarding transactions, including the time they occurred, and the users involved, accessible to anyone.

Blockchain users are identified through addresses, which are strings of numbers and letters very similar to a bank IBAN. This is why Bitcoin transactions are called "pseudo-anonymous," as they are visible to everyone but not attributable to physical persons, rather to virtual identities. To validate a Bitcoin transaction, it must be recognized as correct by most of the network. This occurs through a complex system of Blockchain ledger control, which is updated whenever a user sends or receives Bitcoin. However, this verification process requires a considerable number of mathematical calculations and high energy costs, often carried out with the support of some Blockchain users called miners. These miners voluntarily, through the installation of specific software on their computers, provide the Blockchain with the computing power of their devices and verify the correctness of large groups of transactions (called blocks, hence the name Blockchain). Since this task demands significant energy costs, miners are rewarded by the system: for each validated transaction block, the algorithm generates new Bitcoins to reward miners who have supported the network. This is also the method through which the system introduces new currency into the market, programmed not to exceed twenty-one million units, a figure expected to be reached by 2140

| [11] | Capoti, D., Colacchi, E., & Maggioni, M. (2015). Bitcoin revolution. La moneta digitale alla conquista del mondo. Hoepli. |

[11]

.

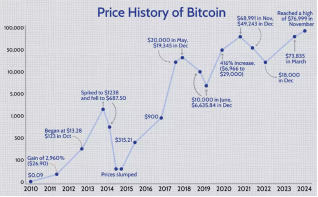

We come to the ultimate question: How much is Bitcoin worth? Without a central body controlling Bitcoin emissions, its exchange rate is determined solely by the market. If at the time of its first issuance, 1 BTC was worth a few cents, by October 2014, its value had risen to $350, by late 2016

| [4] | A. Smith. (1973). Indagine sulla natura e le cause della ricchezza delle nazioni. Arnoldo Mondadori Editore. |

[4]

, it was trading for about $1000, while at the end of 2017, 1 BTC reached approximately $17,000. Furthermore, by January 2022, 1 BTC was worth about $43,000, by July 2024, $66,000, and just five.

6. Bitcoin and Potential Global Impacts

For decades, the dollar has dominated the scene as the world's reserve currency. However, the first cracks in the system are beginning to create such significant fissures that the question is no longer if the system will collapse but when it will and, more importantly, what will happen afterward. For this reason, money as we know it could be supplemented—or even replaced—by a scarce, secure, decentralized digital asset with an unstoppable growth rate (

Figure 1).

During a recent campaign in Nashville, Tennessee, Donald Trump stated his desire for the United States to become the crypto capital of the world and a global Bitcoin superpower. This has reignited discussions about a strategic project that could redefine how governments accumulate sovereign assets through the creation of a national strategic reserve, not in gold or oil but in Bitcoin.

In a few months, Trump transitioned from being one of the harshest critics of a digital asset so devalued it was nicknamed "shit coin" to becoming its biggest supporter. This support was demonstrated not only in words but also in actions: during a meeting with members of the digital resources sector in September 2024, the presidential hopeful visited PubKey, a crypto bar in Manhattan, and purchased what were later named crypto burgers for all campaign participants using Bitcoin (worth $998.77). This gesture, along with his political promises, galvanized the market, fueling expectations of a favorable cryptocurrency framework. Meanwhile, Bitcoin surpassed the $100,000 threshold.

A strategic reserve in Bitcoin could thus prove to be the ultimate solution to sovereign debt sustainability. Reflecting on it, if Bitcoin's value continues to grow over the coming decades, the government could use this reserve to repay part of the public debt, turning a bold gamble into a brilliant move. This refers to the Bitcoin Act, a proposal by Senator Cynthia Lummis, which envisions the U.S. government purchasing and storing large quantities of Bitcoin as a strategic reserve. The plan involves a massive purchase program—up to two hundred thousand Bitcoins per year for five years, totaling a maximum of one million units in reserve—requiring the U.S. to print between two hundred and two hundred fifty billion dollars

.

Msefula et al.

highlight the financial and market risks inherent in Bitcoin’s adoption as legal tender, providing a cautionary perspective relevant to the Bitcoin Act’s ambitious goals. It is thus worth asking: if the U.S. government began purchasing Bitcoin in the quantities proposed by Lummis's plan

, what would happen to the currency's supply and demand? On one hand, consider that the maximum cap for Bitcoin is set at twenty-one million units; on the other, an increase in demand from a giant like the U.S. government could drive the price to unimaginable levels, especially considering that there are just under twenty million units in circulation.

In any case, implementing the program at this historical moment would be crucial, as it would not be merely an economic move but, above all, a geopolitical one. Given that BRICS member countries are creating currencies backed by real assets like gold and natural resources, the United States must react to maintain financial dominance on the global stage

| [20] | Khalfaoui, R., Hammoudeh, S., & Ziaur Reh, M. (2023). Spillovers and connectedness among BRICS stock markets, cryptocurrencies, and uncertainty: Evidence from the quantile vector autoregression network. Emerging Markets Review, Vol. 54(101002). https://doi.org/10.1016/j.ememar.2023.101002 |

[20]

. Why not react by choosing gold? Because Bitcoin has unique qualities: it is finite, immutable, decentralized, and, unlike gold, easily transferable. In short, Bitcoin is digital gold with an intrinsic and uncensorable transactional network to transfer it globally.

In the financial realm, the U.S. government faces one challenge after another, from public debt exceeding thirty-five trillion dollars to rising inflation, from international investor distrust to increasing interest rates crippling banks. In such a scenario, any tool capable of increasing the overall value of national assets would significantly support strengthening the country's financial position. This is where Bitcoin comes into play: with an average annual growth of over sixty percent in the last ten years, Bitcoin has proven to be an asset capable of challenging any other traditional store of value. If the Bitcoin Act is approved, it will not only be a paradigm shift but also a seismic event in global markets, positioning the United States as a leader in Bitcoin reserve management, thereby legitimizing the cryptocurrency as a true sovereign asset.

With the purchase of about five percent of the total Bitcoin supply, considering that the total number of Bitcoins held by all governments worldwide is around 529,000 units, a precedent would be set that could pave the way for similar plans in other countries, especially Italy. The real issue to address is regulatory convergence: each U.S. state has its approach to the world of cryptocurrencies, creating a regulatory mosaic often difficult to navigate, even for the most experienced actors. If the Trump administration indeed aims to transform the U.S. into the hub of the global crypto market—and the intention to appoint a Presidential Advisory Council dedicated to this world is proof of that—we could seriously witness regulatory convergence. This would result in a shift not only for institutional investors but also for top-tier banks, opening the doors to an unprecedented flow of talent and capital, transforming the crypto world from a niche asset to a pillar of global reserves. While Bitcoin offers unique advantages, such as decentralization, transparency, and finite supply, it also faces significant challenges. One critical issue is the high energy consumption associated with its proof-of-work consensus mechanism, which raises environmental concerns. Studies suggest that Bitcoin’s annual energy usage rivals that of some small countries, prompting calls for more sustainable alternatives, such as proof-of-stake systems. Additionally, Bitcoin’s scalability issues hinder its ability to handle a large volume of transactions efficiently. Regulatory challenges further complicate its adoption, as governments worldwide struggle to balance fostering innovation with ensuring financial stability and consumer protection.

Despite these challenges, Bitcoin’s unique attributes such as resistance to censorship and its potential role as a hedge against traditional monetary instability position it as a compelling alternative or complement to fiat currencies. Policymakers and institutions must address these limitations while exploring how Bitcoin can coexist with traditional monetary systems to maximize its benefits.

Beyond these considerations, it should not be forgotten that the cornerstone of cryptocurrencies is that they are technology: their true value is measured not only in terms of price but, above all, in their capacity to innovate, find practical applications in everyday life, and gain legitimacy through clearer and more solid regulations. A revolution is underway, and it is happening before our eyes. The world's great powers are at a historical crossroads concerning the exploration of the future of money, technology, and politics: will they be bold enough to seize this opportunity?

7. The Fei and Bitcoin: Analogies and Considerations

To project into the future, one must understand the past, and to this end, it is fitting to illustrate the history of an ancient civilization in Micronesia, in the western Pacific area, specifically on the island of Yap

. Transactions on the island were conducted using an instrument halfway between commodity money and fiat money; the inhabitants of Yap used limestone discs known as Ray stones (or fei), often taller than a person, with a diameter of up to three meters and weighing up to four tons, with a hole in the center to facilitate transport using large wooden poles

. The Ray stones were quarried from Palau, an island about two hundred ten kilometers from Yap, and transported there by sea on makeshift rafts. Consequently, when a storm arose during transport, the Yapese were forced to throw the discs into the ocean to survive

| [21] | Kula, R. (1991). The Stone Money of Yap: a case study of a Non-Monetary Society. In T. E. Banking. New York: Harper & Row. |

[21]

.

Such a heavy currency with significant logistical challenges was not physically exchanged; instead, ownership was transferred simply through public declaration

| [25] | Malinoski, B. (1992). Argonauts of the Western Pacific. London: Routledge. |

[25]

. This oral tradition was so reliable that even the discs left at the bottom of the ocean became a stable part of the island's economic system. It is reasonable to believe that the oral tradition on Yap constituted a kind of accounting ledger known to all islanders

| [26] | Mankiw, N. G., & Taylor, M. (2011). Macroeconomia. Quinta edizione italiana aggiornata alla settimana edizione americana. |

[26]

. In a small village, after all, knowing how many times the currency was exchanged and who held ownership was within everyone's reach, without the need for a governmental organization or financial intermediary to remember it

.

The concept of shared knowledge is also the basis of the most recent forms of digital currency, such as Bitcoin. In a way, Bitcoin represents a return to valuing the concept of common memory and recording: with Bitcoin, the community once again becomes the custodian of its memory. Appearing on the scene at the end of a severe crisis—the 2008 crisis—that had eroded trust in banking institutions, Bitcoin removed the very protagonists of the crisis from the economic equation inherent in transactions between individuals, creating an alternative monetary system where the community regained the power to control money exchanges without needing an intermediary to guarantee each transaction. But, as a digital currency, how does it achieve this? To understand, one must investigate the technology supporting it. Bitcoin exists thanks to a chain of blocks (better known as Blockchain), which can be imagined here as the automated, digital, and global version of the oral transmission that tracked legal rights over the fei. What Blockchain technology uses to safeguard shared memory are not people but highly sophisticated devices (computers, to be precise) that lend their computing power to process, verify, and finally archive each transaction. The extraordinary aspect of Blockchain is its intrinsic peculiarity of allowing money transfers at any time, as needed, in a few moments and without an intermediary's supervision, redistributing within the community (using Blockchain) the power stripped from the intermediary. Blockchain, in fact, returns full ownership of money to individuals who own a piece of that chain of blocks, and that piece is Bitcoin: by purchasing Bitcoin, one acquires rights over a part of Blockchain technology, and no one can freeze or deprive the holder of that right.

Blockchain technology, the backbone of Bitcoin, reflects a modern iteration of ancient communal accounting systems, such as the Yapese use of fei stones. In both cases, shared community knowledge validates ownership and transactions. The Blockchain’s cryptographic integrity ensures transparency and trust without reliance on centralized intermediaries. Budish

emphasizes that this decentralization addresses the economic challenges of building trust at scale, a fundamental issue in contemporary financial systems. Furthermore, Blockchain’s ability to maintain immutable records has applications beyond finance, including secure voting systems, supply chain management, and digital identity verification, underscoring its transformative potential across industries.

The revolutionary power of this digital currency is so disruptive because it is free and global: like the Internet, Bitcoin and Blockchain belong to no one. Similarly, as the Internet has democratized access to information, it is time for a similar transformation to occur with money. Money is trust, a neutral ambassador that allows two individuals who do not know each other to cooperate through value exchanges. Trust is the true key to understanding money: while it is true that money has been the first great conqueror in history, for which the bloodiest wars have been fought and the most catastrophic economic crises have occurred, it is also incontrovertible that it has functioned (and functions) as a tool of social interaction (and disintermediation of barter over time and space), allowing billions of people—being intrinsically sociable and anthropologically social animals—to cooperate despite not knowing each other, despite the lack of trust between them.

This brings us back to the initial premises: neither the fei nor banknotes possess intrinsic value; the former are not made of precious material, nor are the latter, whose value derives from an invention of the collective imagination in which the entire community has placed trust. Therefore, if money is the medium in which society places trust, the money of the future could legitimately take heterogeneous forms, from stone discs to paper, to pieces of technology, as long as it represents the history and values in which society believes.

In a digital and global information economy, the need for a digital and supranational currency immediately arises, as it is uncontrollable by governmental organizations. Furthermore, in a context where distrust of traditional financial systems is strong, it becomes urgent to be aware of the freedom to use the monetary instrument that best represents the values and principles one relies on, and to understand that although challenging evolving is essential.

8. Conclusions

Bitcoin represents a significant chapter in the ongoing evolution of money, embodying a paradigm shift toward decentralization and digitalization. As a response to the financial vulnerabilities exposed by the 2008 Great Recession, Bitcoin challenges traditional financial systems and redefines trust in monetary transactions. However, its path forward is not without obstacles. Addressing energy inefficiency, improving scalability, and achieving regulatory clarity will be crucial for its broader acceptance.

This event, which disillusioned millions of vulnerable individuals, uncovered the Pandora's box of the U.S. banking system, revealing its irresponsibility, fragility, and injustices. In this distressing context, Bitcoin, with its guarantees of security, transaction control, and decentralization, emerged as a worthy alternative. Bitcoin has presented individuals oppressed by economic turmoil with an escape route from the stringent control of traditional credit institutions. It has done so supported by a technology Blockchain that allows users to conduct transactions where power is equally distributed among the parties involved, without the involvement of intermediaries such as government organizations or financial institutions. A decisive step towards integrating Bitcoin into the traditional economic system is represented by the Bitcoin Act, a plan proposed by American Senator Cynthia Lummis. If approved by the Trump administration, it will not only strengthen the U.S.'s position as a crypto superpower but also redefine the very concept of strategic reserves, legitimizing Bitcoin as a sovereign asset. The transition from fiat money to a form of decentralized digital currency is not so much a matter of technological innovation as it is an unprecedented cultural shift. Bitcoin has found fertile ground among those disillusioned with institutions, aspiring to a more transparent monetary system. Trust, always the foundation of transactions among social animals, is moving away from centralized institutions towards decentralized but transparent systems. This shift inevitably prompts reflections on how modern humans, within a social context, conceive money and what values they want money to reflect. However, treating Bitcoin merely as a response to institutional distrust would diminish the opportunity this digital currency offers the community: to renew the approach to money and economic-financial transactions and embrace a form of currency capable of generating satisfaction for a continuously and rapidly evolving society.

Thus, future research could continue to explore the implications of this financial transformation. Key areas of focus should include the long-term economic impact of widespread cryptocurrency adoption, the potential for regulatory frameworks that balance innovation with financial stability, and the geopolitical consequences of decentralized monetary systems. Additionally, further studies should examine the environmental sustainability of Bitcoin and alternative blockchain consensus mechanisms that could enhance efficiency while maintaining security. A comprehensive, interdisciplinary approach will be essential to fully understanding and anticipating the evolving role of cryptocurrencies in the global financial system.

Abbreviation

PoW | Proof of Work |

EMU | European Economic and Monetary Union |

ECB | European Central Bank |

ESCB | European System of Central Banks |

EU | European Union |

ECSC | European Coal and Steel Community |

CDO | Collateralized Debt Obligations |

Fed | Federal Reserve Bank |

GDP | Gross Domestic Product |

Acknowledgments

This section serves to recognize contributions that do not meet authorship criteria, including technical assistance, donations, or organizational aid. Individuals or organizations should be acknowledged with their full names. The acknowledgments should be placed after the conclusion and before the references section in the manuscript.

Author Contributions

Diego Mazzitelli: Project administration, Writing – original draft, Writing review & editing

Elia Fiorenza: Supervision, Conceptualization, Formal Analysis

Ines Belgacem: Conceptualization, Formal Analysis

Carmelo Arena: Conceptualization, Formal Analysis

Funding

This research is done thanks to the work of the authors who declare that they have not received any public or private funding for its implementation.

Conflicts of Interest

The authors declare no conflicts of interest.

References

| [1] |

European Parliament. Treaty of Rome. Available from:

https://www.europarl.europa.eu/about-parliament/it/in-the-past/the-parliament-and-the-treaties/treaty-of-rome

|

| [2] |

European Parliament. Single European Act. Available from:

https://www.europarl.europa.eu/about-parliament/it/in-the-past/the-parliament-and-the-treaties/single-european-act

|

| [3] |

European Prliament. Treaty of Lisbon. Available from:

https://www.europarl.europa.eu/about-parliament/it/in-the-past/the-parliament-and-the-treaties/treaty-of-lisbon

|

| [4] |

A. Smith. (1973). Indagine sulla natura e le cause della ricchezza delle nazioni. Arnoldo Mondadori Editore.

|

| [5] |

Angell, N. (1929). The Story of Money. New York: Frederick A. Stokes Company.

|

| [6] |

Ballester, L., González-Urteaga, A., & Shen, L. (n.d.). Green bond issuance and credit risk: International evidence. Journal of International Financial Markets, Institutions and Money, Volume 94(102013).

https://doi.org/10.1016/j.intfin.2024.102013

|

| [7] |

Banca d'Italia. (2016). Relazione Annuale 2015. Roma: Divisione Editoria e stampa.

https://www.bancaditalia.it/pubblicazioni/relazione-annuale/2015/rel_2015.pdf

|

| [8] |

Bitcoin's Price History.

https://www.investopedia.com/articles/forex/121815/bitcoins-price-history.asp

|

| [9] |

Budish, E. (2025). Trust of scale: The economic limits of cryptocurrencies. The Quaterly Journal of Economics, Vol. 140(1), Pages 1-62.

https://doi.org/10.1093/qje/qjae033

|

| [10] |

C. Lummis. (2024). Bitcoin Act: A proposal for a strategic Reserve. Retrieved from

https://www.congress.gov/bill/118th-congress/senate-bill/4912

|

| [11] |

Capoti, D., Colacchi, E., & Maggioni, M. (2015). Bitcoin revolution. La moneta digitale alla conquista del mondo. Hoepli.

|

| [12] |

Chey, H. (2023). Cryptocurrencies and the IPE of money; an agenda for research. Review of International Political Economy.

https://doi.org/10.1080/09692290.2022.2109188

|

| [13] |

Chibane, M., & Janson, N. (2025). Is Bitcoin the best safe haven against geopolitical risk? Finance Research Letters, Volume 74(106543).

https://doi.org/10.1016/j.frl.2024.106543

|

| [14] |

Cicchiello, A. F., Cotugno, M., Monferrà, S., & Perdichizzi, S. (2022). Which are the factors influencing green bonds issuance? Evidence from the European bonds market. Finance Research Letters, Volume 50(103190).

https://doi.org/10.1016/j.frl.2022.103190

|

| [15] |

Comandini, G. (2021). Da Zero alla Luna - Quando, come, perché la blockchain sta cambiando il mondo. II edizione ampliata, Pages 53-65.

|

| [16] |

EUR-Lex. (1951, Aprile 18). Retrieved from Trattato di Parigi:

https://www.europarl.europa.eu/about-parliament/it/in-the-past/the-parliament-and-the-treaties/treaty-of-paris

|

| [17] |

European Parlament.

https://www.europarl.europa.eu/about-parliament/it/in-the-past/the-parliament-and-the-treaties/maastricht-treaty

|

| [18] |

Friedman, M. (1960). A program for monetary stability. New York: Fordham University Press.

|

| [19] |

Gorton, G. (2010). Slapped by the Invisible Hand: The panic of 2007 (Financial Management Association Survey and Synthesis ed.). Oxford University Press.

|

| [20] |

Khalfaoui, R., Hammoudeh, S., & Ziaur Reh, M. (2023). Spillovers and connectedness among BRICS stock markets, cryptocurrencies, and uncertainty: Evidence from the quantile vector autoregression network. Emerging Markets Review, Vol. 54(101002).

https://doi.org/10.1016/j.ememar.2023.101002

|

| [21] |

Kula, R. (1991). The Stone Money of Yap: a case study of a Non-Monetary Society. In T. E. Banking. New York: Harper & Row.

|

| [22] |

Levant, Y., & Nikitin, M. (2020). History of an unsuccessful performance measurement innovation: surplus accounts in France (1966–c.1990). Accounting History Review, 30(3), 307-339.

https://doi.org/10.1080/21552851.2020.1810722

|

| [23] |

Levulytė, L., & Šapkauskienė, A. (2021). Cryptocurrency in context of fiat money functions. The Quarterly Review of Economics and Finance, Volume 82, Pages 44-54.

https://doi.org/10.1016/j.qref.2021.07.003

|

| [24] |

Lim, K., Liu, C., & Zhang, S. (2024). Optimal central banking policies: Envisioning the post-digital yuan economy with loan prime rate-setting. Emerging Markets Review, Vol. 59(101108).

https://doi.org/10.1016/j.ememar.2024.101108

|

| [25] |

Malinoski, B. (1992). Argonauts of the Western Pacific. London: Routledge.

|

| [26] |

Mankiw, N. G., & Taylor, M. (2011). Macroeconomia. Quinta edizione italiana aggiornata alla settimana edizione americana.

|

| [27] |

Miller, C. (2021). Retrieved from

https://coingeek.com/stuart-haber-and-scott-stornetta-how-our-timestamping-mechanism-was-used-in-bitcoin-video/

|

| [28] |

Morris, R. J. (2012). Men, women and money. Perspectives on gender, wealth and investment, 1850–1930. Accounting History Review, 22(3), 307-309.

https://doi.org/10.1080/21552851.2012.724910

|

| [29] |

Msefula, G., Hou, T., & Lemesi, T. (2024). Financial and market risks of bitcoin adoption as legal tender. Evidence from El Salvador (Vol. 11(1)). Humanities and Social Sciences Communications.

https://doi.org/10.1057/s41599-024-03908-3

|

| [30] |

Paul, E. (1966). The Stone Money of Yap. In Primitive Money (Second Edition) (pp. Pages 36-40). Pergamon: Einzig Paul.

https://doi.org/10.1016/B978-0-08-011679-2.50013-9

|

| [31] |

Persson, M. E. (2016). The social life of money. Accounting History Review, 26(1), 45-49.

https://doi.org/10.1080/21552851.2015.1128167

|

| [32] |

Radford, R. (1945). The Economic Organisation of a P. O. W. Camp (Vol. Vol 12). Economica.

https://doi.org/10.2307/2550133

|

| [33] |

Razavi, R., & Elbahnasawy, N. (2025). Unlocking credit access: Using non-CDR mobile data to enhance credit scoring for financial inclusion. Finance Research Letters, Vol. 73(106682).

https://doi.org/10.1016/j.frl.2024.106682

|

| [34] |

Roubini, N., & Mihm, S. (2010). Crisis Economics: a crash course in the future of finance. New York: Penguin Books.

|

| [35] |

Satoshi, N. (2008). Bitcoin: A peer-to-peer electronic cash system. Retrieved from

https://static.upbitcare.com/931b8bfc-f0e0-4588-be6e-b98a27991df1.pdf

|

| [36] |

Signorelli, A. D. (2024). Crypto. Retrieved from Wired:

https://www.wired.it/article/bitcoin-el-salvador-bukele-bhutan

|

| [37] |

Smith, A. (1776). The Wealth of Nations. Londra: Methuen & Co. Ltd. Retrieved from

https://www.rrojasdatabank.info/Wealth-Nations.pdf

|

| [38] |

Stanciu, A., Partsch, M., & Lechner, C. (2024). Basic Human Values and adoption of cryptocurrency. (Vol. Vol. 15). Frontiers in Psychology.

https://doi.org/10.3389/fpsyg.2024.1395674

|

| [39] |

Varallo. (2024). Retrieved

https://www.cambiovarallo.it/storia.htm

|

| [40] |

Weineer, A. B. (1992). The meaning of Money: The role of Money in the Economy. University of Hawai.

|

| [41] |

Zohar, A. (2015). Bitcoin: under the hood. Communications of The ACM, Pages 104-113.

https://dl.acm.org/doi/10.1145/2701411

|

Cite This Article

-

APA Style

Mazzitelli, D., Fiorenza, E., Belgacem, I., Arena, C. (2025). Relevance of the Ancient Barter Technique in Currency Exchange: From the Euro to Bitcoin. International Journal of Economics, Finance and Management Sciences, 13(2), 49-60. https://doi.org/10.11648/j.ijefm.20251302.11

Copy

|

Copy

|

Download

Download

ACS Style

Mazzitelli, D.; Fiorenza, E.; Belgacem, I.; Arena, C. Relevance of the Ancient Barter Technique in Currency Exchange: From the Euro to Bitcoin. Int. J. Econ. Finance Manag. Sci. 2025, 13(2), 49-60. doi: 10.11648/j.ijefm.20251302.11

Copy

|

Download

AMA Style

Mazzitelli D, Fiorenza E, Belgacem I, Arena C. Relevance of the Ancient Barter Technique in Currency Exchange: From the Euro to Bitcoin. Int J Econ Finance Manag Sci. 2025;13(2):49-60. doi: 10.11648/j.ijefm.20251302.11

Copy

|

Download

-

@article{10.11648/j.ijefm.20251302.11,

author = {Diego Mazzitelli and Elia Fiorenza and Ines Belgacem and Carmelo Arena},

title = {Relevance of the Ancient Barter Technique in Currency Exchange: From the Euro to Bitcoin

},

journal = {International Journal of Economics, Finance and Management Sciences},

volume = {13},

number = {2},

pages = {49-60},

doi = {10.11648/j.ijefm.20251302.11},

url = {https://doi.org/10.11648/j.ijefm.20251302.11},

eprint = {https://article.sciencepublishinggroup.com/pdf/10.11648.j.ijefm.20251302.11},

abstract = {Objective of this manuscript is both to tracing the evolution of money, and examining its transition from commodity money to fiat money, up to the emergence of cryptocurrencies. It highlights the inherent issues of the barter system, emphasizing the urgencies and necessities that favored the adoption of legal tender. Subsequently, the impact of the creation of the Euro on the European economy—both historically and geopolitically—will be analyzed, contextualizing the European Union's institutional process. In a response to the crisis, Bitcoin (the first decentralized cryptocurrency) will be introduced, along with an illustration of the supporting Blockchain technology will be provided. Finally, the proposal of American Senator Lummis, who suggests a massive purchase of Bitcoin to be used as a strategic reserve through the “Bitcoin Act” program, will be explored, prompting several reflections on the future of the petrodollar as a reserve instrument. Through these reflections, the reader could develop their own thoughts on the importance of evolving towards forms of money more suited to an increasingly digitized and decentralized economy. In conclusion, by proposing an analogy between the ancient monetary practices on Yap and cryptocurrencies, we aim to stimulate the reflection that innovation is not only desirable in this fast-paced world but essential.

},

year = {2025}

}

Copy

|

Download

-

TY - JOUR

T1 - Relevance of the Ancient Barter Technique in Currency Exchange: From the Euro to Bitcoin

AU - Diego Mazzitelli

AU - Elia Fiorenza

AU - Ines Belgacem

AU - Carmelo Arena

Y1 - 2025/04/10

PY - 2025

N1 - https://doi.org/10.11648/j.ijefm.20251302.11

DO - 10.11648/j.ijefm.20251302.11

T2 - International Journal of Economics, Finance and Management Sciences

JF - International Journal of Economics, Finance and Management Sciences

JO - International Journal of Economics, Finance and Management Sciences

SP - 49

EP - 60

PB - Science Publishing Group

SN - 2326-9561

UR - https://doi.org/10.11648/j.ijefm.20251302.11

AB - Objective of this manuscript is both to tracing the evolution of money, and examining its transition from commodity money to fiat money, up to the emergence of cryptocurrencies. It highlights the inherent issues of the barter system, emphasizing the urgencies and necessities that favored the adoption of legal tender. Subsequently, the impact of the creation of the Euro on the European economy—both historically and geopolitically—will be analyzed, contextualizing the European Union's institutional process. In a response to the crisis, Bitcoin (the first decentralized cryptocurrency) will be introduced, along with an illustration of the supporting Blockchain technology will be provided. Finally, the proposal of American Senator Lummis, who suggests a massive purchase of Bitcoin to be used as a strategic reserve through the “Bitcoin Act” program, will be explored, prompting several reflections on the future of the petrodollar as a reserve instrument. Through these reflections, the reader could develop their own thoughts on the importance of evolving towards forms of money more suited to an increasingly digitized and decentralized economy. In conclusion, by proposing an analogy between the ancient monetary practices on Yap and cryptocurrencies, we aim to stimulate the reflection that innovation is not only desirable in this fast-paced world but essential.

VL - 13

IS - 2

ER -

Copy

|

Download