The current study investigates the factors which determine the usage of e-payments in Gangtok district, Sikkim, which is an emerging urban economy in India. By incorporating the concept of trust into TAM (Technology Acceptance Model), this research aims to find out whether perceived usability, perceived utility and trust can affect users' behavioural intentions to utilize e-payment services. Data were gathered through a survey questionnaire distributed among 384 participants selected randomly through stratification in order to represent different demographics and occupations. To examine the relationships proposed in the hypotheses, structural equation modelling (SEM) was used. All five hypotheses (H1-H5) have been found to be statistically significant. Therefore, these results confirm that trust will positively affect the perceptions of usability and utility; and therefore, is a very important precursor in the process of adopting digital payments. Perceived usability has a positive and significant impact on perceptions of usability and on behavioural intent. Additionally, there is a strong positive correlation between perceptions of utility and users' intentions to adopt e-payment services, while also being a partial mediator between perceptions of usability and users' intentions to adopt e-payment services. The research highlights that in semi-urban and emerging urban environments, usability, perceived benefits, and trust, are major determinants of the utilization of electronic payment services. In terms of policy recommendations, this study suggests that governments should provide support for the development of digital infrastructure, increase financial education, encourage public awareness about how to protect against security threats and fraud prevention, as well as create user friendly interfaces for digital payment services to enhance the rate of adoption.

| Published in | International Journal of Economics, Finance and Management Sciences (Volume 14, Issue 2) |

| DOI | 10.11648/j.ijefm.20261402.16 |

| Page(s) | 173-183 |

| Creative Commons |

This is an Open Access article, distributed under the terms of the Creative Commons Attribution 4.0 International License (http://creativecommons.org/licenses/by/4.0/), which permits unrestricted use, distribution and reproduction in any medium or format, provided the original work is properly cited. |

| Copyright |

Copyright © The Author(s), 2026. Published by Science Publishing Group |

TAM, Trust, Perceived Ease of Use, Perceived Usefulness, Electronic Payment System

Sl.No. | Particulars | No. of items | Cronbach’s Alpha |

|---|---|---|---|

1 | Trust | 5 | 0.825 |

2 | Perceived Usefulness | 5 | 0.858 |

3 | Perceived ease of use | 5 | 0.853 |

4 | Intention to Use | 5 | 0.865 |

Kaiser-Meyer-Olkin Measure of Sampling Adequacy | 0.950 |

Bartlett's Test of Sphericity Approx. Chi-Square | 2467.533 |

DF | 190 |

Sig | 0.000 |

Variable | Frequency | Percent |

|---|---|---|

Gender | ||

Male | 207 | 53.91 |

Female | 177 | 46.09 |

Total | 384 | 100.0 |

Age | ||

Below 30 | 101 | 26.3 |

30 – 40 | 114 | 29.7 |

41 – 50 | 95 | 24.7 |

Above 50 | 74 | 19.3 |

Total | 384 | 100.0 |

Occupation | ||

Government sector employee | 84 | 21.9 |

Private sector Employee | 79 | 20.6 |

Student | 70 | 18.2 |

Business | 87 | 22.7 |

Agricultural | 64 | 16.7 |

Total | 384 | 100.0 |

E-Payment Methods | ||

Credit Card | 81 | 21.1 |

Debit Card | 129 | 33.6 |

Internet Banking | 86 | 22.4 |

Mobile Wallets | 88 | 22.9 |

Total | 384 | 100.0 |

Indices | Value | Suggested value |

|---|---|---|

Chi-square value | 0.726 | - |

DF | 1 | - |

P value | 0.394 | > 0.05 |

Chi-square value/DF | .726 | < 5.00 |

GFI | 0.999 | > 0.90 |

AGFI | 0.985 | > 0.90 |

NFI | 0.999 | > 0.90 |

CFI | 1.00 | > 0.90 |

RMR | 0.084 | < 0.08 |

RMSEA | 0.000 | < 0.08 |

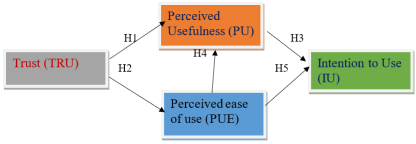

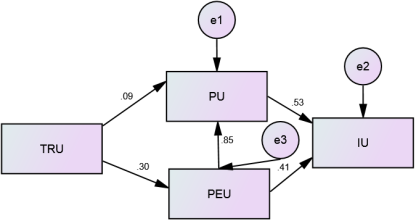

Hypothesis | S.E. | C.R. | P | Results | |||

|---|---|---|---|---|---|---|---|

H1 | PU | <--- | TRU | .062 | 2.939 | .003 | Significant P 0.01 |

H2 | PEU | <--- | TRU | .117 | 4.933 | *** | Significant P 0.001 |

H3 | IU | <--- | PU | .053 | 9.702 | *** | Significant P≤0.001 |

H4 | PU | <--- | PEU | .032 | 27.507 | *** | Significant P≤0.001 |

H5 | IU | <--- | PEU | .055 | 7.378 | *** | Significant P0.001 |

AGFI | Adjusted Goodness-of-Fit Index |

AMOS | Analysis of Moment Structures |

AVE | Average Variance Extracted |

CFI | Comparative Fit Index |

CR | Composite Reliability |

DF | Degrees of Freedom |

EPS | Electronic Payment Systems |

GFI | Goodness-of-Fit Index |

ICT | Information and Communication Technology |

IS | Information Systems |

IU | Intention to Use |

KMO | Kaiser-Meyer-Olkin Measure of Sampling Adequacy |

NFI | Normed Fit Index |

PEOU | Perceived Ease of Use |

PU | Perceived Usefulness |

RMSEA | Root Mean Square Error of Approximation |

RMR | Root Mean Square Residual |

SEM | Structural Equation Modelling |

TAM | Technology Acceptance Model |

TPB | Theory of Planned Behaviour |

TRU | Trust |

UTAUT | Unified Theory of Acceptance and Use of Technology |

| [1] | Abbas, S., Mehmood, B., Ahmad, A., & Khan, M. A. (2025). Integrating technology acceptance and fintech innovation factors to examine digital payment adoption and financial inclusion. Journal of Financial Services Marketing, 30(1), 45–60. |

| [2] | Aburbeian, A. M., Owda, A. Y., & Owda, M. (2022). A Technology Acceptance Model survey of the Metaverse prospects. AI, 3(2), 285–302. |

| [3] | Acharya, V., Junare, S. O., & Gadhavi, D. D. (2019). E-payment: Buzz word or reality. International Journal of Recent Technology and Engineering, 8(3S2), 397-404. |

| [4] | Akpınar, E., & Atak, M. (2025). Determinants of digital payment adoption in smart city ecosystems: An extended TAM approach. Technological Forecasting and Social Change, 198, 123456. |

| [5] | Aparna, R. (2024). Adoption of UPI-based digital payments among street vendors in India: An extended technology acceptance model. International Journal of Bank Marketing, 42(2), 289–307. |

| [6] | Azmi, A., Ang, Y. D., & Talib, S. A. (2016). Trust and justice in the adoption of a welfare e-payment system. Transforming Government: People, Process and Policy. |

| [7] | Bajpai, N., Biberman, J., & Sachs, J. D. (2018). Post-Demonetization E-Payment Trends. |

| [8] | Chauhan, M., Shingari, I., & Shingari, I. (2017). Future of e-Wallets: A perspective from under graduates’. International Journal of Advanced Research in Computer Science and Software Engineering, 7(8), 146. |

| [9] | Chen, Y. H., & Barnes, S. (2007). Initial trust and online buyer behaviour. Industrial Management & Data Systems. |

| [10] | Chin, Y. L., Mohd Suki, N., & Ibrahim, A. (2005). Determinants of intention to use an online bill payment system among MBA students. E-Business, (9), 80–91. |

| [11] | Davis, F. D., Bagozzi, R. P., & Warshaw, P. R. (1989). User acceptance of computer technology: A comparison of two theoretical models. Management science, 35(8), 982-1003. |

| [12] | Davis, F. D. (1989). Perceived usefulness, perceived ease of use, and user acceptance of information technology. MIS Quarterly, 13(3), 319–340. |

| [13] | Dmour, A., Brghuthi, R., & Aldmour, R. (2021). Technology acceptance dynamics and adoption of e-payment systems: Empirical evidence from Jordan. International Journal of E-Business Research, 17(2), 61–80. |

| [14] | Dutot, V. (2015). Factors influencing near field communication (NFC) adoption: An extended TAM approach. The Journal of High Technology Management Research, 26(1), 45–57. |

| [15] | Gefen, D., Karahanna, E., & Straub, D. W. (2003). Trust and TAM in online shopping: An integrated model. MIS Quarterly, 27(1), 51–90. |

| [16] | Guriting, P., & Ndubisi, N. O. (2006). Borneo online banking: Evaluating customer perceptions and behavioural intention. Management Research News. |

| [17] | Hair, J. F., Anderson, R. E., Tatham, R. L., & Black, W. C. (1998). Multivariate data analysis (5th ed.). Prentice Hall. |

| [18] |

Hair, J. F., Black, W. C., Babin, B. J., Anderson, R. E., & Tatham, R. L. (2006). Multivariate data analysis (6th ed.). Pearson Prentice Hall.

https://www.scirp.org/reference/ReferencesPapers?ReferenceID=1385913 |

| [19] | Hamid, A. A., Razak, F. Z. A., Bakar, A. A., & Abdullah, W. S. W. (2016). The effects of perceived usefulness and perceived ease of use on continuance intention to use e-government. Procedia Economics and Finance, 35, 644–649. |

| [20] | Hu, L. T., & Bentler, P. M. (1999). Cutoff criteria for fit indexes in covariance structure analysis: Conventional criteria versus new alternatives. Structural Equation Modeling: A Multidisciplinary Journal, 6(1), 1–55. |

| [21] |

Kabir, M. A., Saidin, S. Z., & Ahmi, A. (2015). Adoption of e-payment systems: A review of literature. In Proceedings of the International Conference on E-commerce (Vol. 2012, pp. 112–120).

https://aidi-ahmi.com/download/publication/2015_ICoEC_kabir_saidin_ahmi.pdf |

| [22] | Kim, C., Tao, W., Shin, N., & Kim, K. S. (2010). An empirical study of customers’ perceptions of security and trust in e-payment systems. Electronic Commerce Research and Applications, 9(1), 84–95. |

| [23] | Lai, P. C. (2017). Security as an extension to TAM model: Consumers’ intention to use a single platform e-payment. Asia-Pacific Journal of Management Research and Innovation, 13(3–4), 110–119. |

| [24] | Lai, P. C., & Ahmad, Z. A. (2014). Perceived enjoyment of Malaysian consumers’ intention to use a single platform E-payment. In International Conference on Liberal Arts & Social Sciences, 25th–29th April. |

| [25] | Lai, P. C., & Zainal, A. A. (2015). Consumers’ intention to use a single platform e-payment system: A study among Malaysian internet and mobile banking users. Journal of Internet Banking and Commerce, 20(1), 1–13. |

| [26] | Linh, N. T., & Huyen, P. T. (2025). Extending the trust-based technology acceptance model with TPB to explain digital payment intention. Asia Pacific Journal of Marketing and Logistics, 37(1), 88–106. |

| [27] | Lolowang, J., Tumiwa, R. A. F., & Rantung, G. C. (2024). Mobile payment adoption among MSMEs: The mediating role of perceived usefulness. Journal of Asian Business and Economic Studies, 31(3), 215–232. |

| [28] | Mogaji, E., Viglia, G., Srivastava, P., & Dwivedi, Y. K. (2024). Is it the end of the technology acceptance model in the era of generative artificial intelligence? International Journal of Contemporary Hospitality Management, 36(10), 3324–3339. |

| [29] | Moon, J. W., & Kim, Y. G. (2001). Extending the TAM for a World-Wide-Web context. Information & Management, 38(4), 217–230. |

| [30] | Nguyen, T. D., & Huynh, P. A. (2018). The roles of perceived risk and trust on e-payment adoption. In International Econometric Conference of Vietnam (pp. 926–940). Springer, Cham. |

| [31] | Nguyen, T. T., Le, H. Q., Pham, M. T., & Tran, D. T. (2024). Factors influencing the adoption of point-of-sale electronic payment systems: An integrated UTAUT–TAM approach. Electronic Commerce Research, 24(4), 1121–1145. |

| [32] | Nguyen, T. T., Tran, T. N. H., Do, T. H. M., Dinh, T. K. L., Nguyen, T. U. N., & Dang, T. M. K. (2024). Digital literacy, online security behaviors and E-payment intention. Journal of Open Innovation: Technology, Market, and Complexity, 10(2), 100292. |

| [33] | Prasetyo, Y. T., Senoro, D. B., German, J. D., & Ong, A. K. S. (2025). Examining system quality and usability in digital payment adoption using an extended TAM. Journal of Retailing and Consumer Services, 78, 103612. |

| [34] | Ramos-de-Luna, I., Montoro-Ríos, F., & Liébana-Cabanillas, F. (2016). Determinants of the intention to use NFC technology as a payment system: An acceptance model approach. Information Systems and e-Business Management, 14(2), 293–314. |

| [35] | Rashid, A., Singh, R., & Verma, S. (2025). Determinants of digital payment adoption in rural India: The mediating role of trust. Journal of Rural Studies, 103, 214–224. |

| [36] | Raza, S. A., Umer, A., & Shah, N. (2017). New determinants of ease of use and perceived usefulness for mobile banking adoption. International Journal of Electronic Customer Relationship Management, 11(1), 44–65. |

| [37] | Salloum, S. A., & Al-Emran, M. (2018). Factors affecting the adoption of e-payment systems by university students: Extending the TAM with trust. International Journal of Electronic Business, 14(4), 371–390. |

| [38] | Santouridis, I., & Kyritsi, M. (2014). Investigating the determinants of internet banking adoption in Greece. Procedia Economics and Finance, 9, 501–510. |

| [39] | Shih, H. P. (2004). Extended technology acceptance model of internet utilization behavior. Information & Management, 41(6), 719–730. |

| [40] | Singh, P., Supriya, N., & Joshna, M. S. (2013). Issues and challenges of electronic payment systems. International Journal for Research in Management and Pharmacy, 2(9), 25–30. |

| [41] | Sinha, I., & Mukherjee, S. (2016). Acceptance of technology, related factors in use of off branch e-banking: An Indian case study. The Journal of High Technology Management Research, 27(1), 88–100. |

| [42] | Sumaya, F., Rahman, M. S., & Hossain, M. A. (2025). Trust, security, and facilitating conditions in electronic payment adoption: Evidence from emerging economies. Information Development, 41(1), 98–112. |

| [43] | Tella, A., & Olasina, G. (2014). Predicting users' continuance intention toward e-payment system: An extension of the technology acceptance model. International Journal of Information Systems and Social Change, 5(1), 47–67. |

| [44] | Teoh, W. M. Y., Chong, S. C., Lin, B., & Chua, J. W. (2013). Factors affecting consumers' perception of electronic payment: An empirical analysis. Internet Research. |

| [45] | Upadhyay, P., & Jahanyan, S. (2016). Analyzing user perspective on the factors affecting use intention of mobile based transfer payment. Internet Research. |

| [46] | Utomo, P., Wibowo, S. F., & Nugroho, A. (2024). Determinants of electronic payment system usage in emerging markets: An empirical investigation. Journal of Business Research, 168, 114052. |

| [47] | Van der Heijden, H. (2003). Factors influencing the usage of websites: The case of a generic portal in The Netherlands. Information & Management, 40(6), 541–549. |

| [48] | Vorm, E. S., & Combs, D. J. (2022). Integrating transparency, trust, and acceptance: The intelligent systems technology acceptance model (ISTAM). International Journal of Human–Computer Interaction, 38(18–20), 1828–1845. |

APA Style

Kafley, G. S., Sahoo, T. K., Faiyyaz, A. G., Giri, G. (2026). Adoption of Electronic Payment Systems in an Emerging Urban Economy: A Technology Acceptance Model Perspective. International Journal of Economics, Finance and Management Sciences, 14(2), 173-183. https://doi.org/10.11648/j.ijefm.20261402.16

ACS Style

Kafley, G. S.; Sahoo, T. K.; Faiyyaz, A. G.; Giri, G. Adoption of Electronic Payment Systems in an Emerging Urban Economy: A Technology Acceptance Model Perspective. Int. J. Econ. Finance Manag. Sci. 2026, 14(2), 173-183. doi: 10.11648/j.ijefm.20261402.16

@article{10.11648/j.ijefm.20261402.16,

author = {Ghana Shyam Kafley and Tapas Kumar Sahoo and Abdul Ghani Faiyyaz and Goutam Giri},

title = {Adoption of Electronic Payment Systems in an Emerging Urban Economy: A Technology Acceptance Model Perspective},

journal = {International Journal of Economics, Finance and Management Sciences},

volume = {14},

number = {2},

pages = {173-183},

doi = {10.11648/j.ijefm.20261402.16},

url = {https://doi.org/10.11648/j.ijefm.20261402.16},

eprint = {https://article.sciencepublishinggroup.com/pdf/10.11648.j.ijefm.20261402.16},

abstract = {The current study investigates the factors which determine the usage of e-payments in Gangtok district, Sikkim, which is an emerging urban economy in India. By incorporating the concept of trust into TAM (Technology Acceptance Model), this research aims to find out whether perceived usability, perceived utility and trust can affect users' behavioural intentions to utilize e-payment services. Data were gathered through a survey questionnaire distributed among 384 participants selected randomly through stratification in order to represent different demographics and occupations. To examine the relationships proposed in the hypotheses, structural equation modelling (SEM) was used. All five hypotheses (H1-H5) have been found to be statistically significant. Therefore, these results confirm that trust will positively affect the perceptions of usability and utility; and therefore, is a very important precursor in the process of adopting digital payments. Perceived usability has a positive and significant impact on perceptions of usability and on behavioural intent. Additionally, there is a strong positive correlation between perceptions of utility and users' intentions to adopt e-payment services, while also being a partial mediator between perceptions of usability and users' intentions to adopt e-payment services. The research highlights that in semi-urban and emerging urban environments, usability, perceived benefits, and trust, are major determinants of the utilization of electronic payment services. In terms of policy recommendations, this study suggests that governments should provide support for the development of digital infrastructure, increase financial education, encourage public awareness about how to protect against security threats and fraud prevention, as well as create user friendly interfaces for digital payment services to enhance the rate of adoption.},

year = {2026}

}

TY - JOUR T1 - Adoption of Electronic Payment Systems in an Emerging Urban Economy: A Technology Acceptance Model Perspective AU - Ghana Shyam Kafley AU - Tapas Kumar Sahoo AU - Abdul Ghani Faiyyaz AU - Goutam Giri Y1 - 2026/04/25 PY - 2026 N1 - https://doi.org/10.11648/j.ijefm.20261402.16 DO - 10.11648/j.ijefm.20261402.16 T2 - International Journal of Economics, Finance and Management Sciences JF - International Journal of Economics, Finance and Management Sciences JO - International Journal of Economics, Finance and Management Sciences SP - 173 EP - 183 PB - Science Publishing Group SN - 2326-9561 UR - https://doi.org/10.11648/j.ijefm.20261402.16 AB - The current study investigates the factors which determine the usage of e-payments in Gangtok district, Sikkim, which is an emerging urban economy in India. By incorporating the concept of trust into TAM (Technology Acceptance Model), this research aims to find out whether perceived usability, perceived utility and trust can affect users' behavioural intentions to utilize e-payment services. Data were gathered through a survey questionnaire distributed among 384 participants selected randomly through stratification in order to represent different demographics and occupations. To examine the relationships proposed in the hypotheses, structural equation modelling (SEM) was used. All five hypotheses (H1-H5) have been found to be statistically significant. Therefore, these results confirm that trust will positively affect the perceptions of usability and utility; and therefore, is a very important precursor in the process of adopting digital payments. Perceived usability has a positive and significant impact on perceptions of usability and on behavioural intent. Additionally, there is a strong positive correlation between perceptions of utility and users' intentions to adopt e-payment services, while also being a partial mediator between perceptions of usability and users' intentions to adopt e-payment services. The research highlights that in semi-urban and emerging urban environments, usability, perceived benefits, and trust, are major determinants of the utilization of electronic payment services. In terms of policy recommendations, this study suggests that governments should provide support for the development of digital infrastructure, increase financial education, encourage public awareness about how to protect against security threats and fraud prevention, as well as create user friendly interfaces for digital payment services to enhance the rate of adoption. VL - 14 IS - 2 ER -

Department of Commerce, SRM University, Sikkim, India

Faculty of Management and Commerce, Ramaiah University of Applied Sciences, Bengaluru, India

Department of Commerce, SRM University, Sikkim, India

Department of Commerce, Jadu Nath College, Odisha, India

Information