The proliferation of mobile money services in Uganda since 2009 has transformed the financial landscape, though limited empirical research has examined their contribution to economic growth. This study investigated the impact of mobile money usage on economic growth in Uganda, focusing on transaction efficiency, financial inclusion, employment generation, and savings mobilization. Grounded in pragmatism as the guiding research philosophy, the study employed a survey, descriptive, and correlational designs across four selected districts. The target sample comprised 385 respondents, with 336 (87.3%) successfully reached, including mobile money agents, agent bankers, commercial bank staff, telecom company representatives, fintech entrepreneurs, regulators, and end-users selected through simple random, purposive, and convenience sampling. Data collection utilized structured questionnaires, key informant interviews, and documentary review of reports from the Bank of Uganda, Uganda Bureau of Statistics, and Uganda Communications Commission. Quantitative data were analyzed using SPSS version 30 through descriptive statistics, and Pearson correlation, while qualitative data underwent thematic analysis. Results revealed that mobile money usage significantly contributes to economic growth through multiple channels: 83.6% of respondents used mobile money as their primary digital finance platform, with 92.0% engaging in daily transactions. The findings showed that a unit change in mobile money usage would result in a 0.339 change in economic growth. The study concludes that mobile money significantly drives Uganda’s economic growth by enhancing financial inclusion, transactional efficiency, remittance flows, and employment generation with a regression model: Economic Growth = 3.105 + 0.339 (Mobile Money Usage. Recommendations include expanding digital infrastructure, strengthening consumer protection against fraud, integrating mobile money with formal taxation systems, and promoting digital financial literacy programs to maximize mobile money’s contribution to Uganda’s economic growth.

| Published in | International Journal of Finance and Banking Research (Volume 12, Issue 3) |

| DOI | 10.11648/j.ijfbr.20261203.11 |

| Page(s) | 60-74 |

| Creative Commons |

This is an Open Access article, distributed under the terms of the Creative Commons Attribution 4.0 International License (http://creativecommons.org/licenses/by/4.0/), which permits unrestricted use, distribution and reproduction in any medium or format, provided the original work is properly cited. |

| Copyright |

Copyright © The Author(s), 2026. Published by Science Publishing Group |

Mobile Money, Economic Growth, Digital Finance, Cashless Economy, Fintech

Respondents’ Data | Attributes | Frequency | Percentage |

|---|---|---|---|

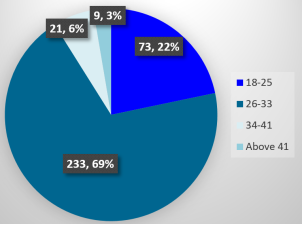

Gender of the Respondents | Male | 219 | 65.2% |

Female | 117 | 34.8% | |

Total | 336 | 100 |

Employment Status | Number | Percentage |

|---|---|---|

Employed | 194 | 57.70% |

Unemployed | 6 | 1.80% |

Self employed | 136 | 40.50% |

Total | 336 | 100.00% |

Nature of Business | Number | Percentage |

|---|---|---|

School | 26 | 7.7% |

Health Centre | 14 | 4.2% |

Fuel station | 46 | 13.7% |

Restaurant/Hotel | 15 | 4.5% |

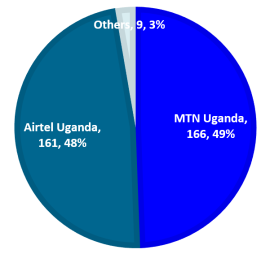

Agent Banking | 69 | 20.5% |

Mobile Money Agent | 166 | 49.4% |

Total | 336 | 100 |

Nature of Digital Finance | Number | Percentage |

|---|---|---|

Mobile Money | 281 | 83.6% |

School Pay Platform | 16 | 4.8% |

Visa card/Mastercard/Credit Card | 25 | 7.4% |

Mobile Banking | 6 | 1.8% |

Cryptocurrency | 8 | 2.4% |

Total | 336 | 100 |

Frequency | Number | Percentage |

|---|---|---|

Very Rarely | 4 | 1.2% |

Rarely | 3 | 0.9% |

Not much/moderately | 20 | 6.0% |

Often | 129 | 38.4% |

Very Often | 180 | 53.6% |

Total | 336 | 100 |

Utility Type | Number | Percentage |

|---|---|---|

School fees | 113 | 33.6% |

Water | 68 | 20.2% |

Electricity | 137 | 40.8% |

TV subscription | 10 | 3.0% |

Fuel | 5 | 1.5% |

Others | 3 | 0.9% |

Total | 336 | 100.0% |

Service Type | Number | Percentage |

|---|---|---|

Online Shopping | 9 | 2.7% |

Saving | 20 | 6.0% |

Sending and Receiving Money | 228 | 67.9% |

Loan/credit acquisition and payment | 51 | 15.2% |

Investment | 13 | 3.9% |

Insurance | 11 | 3.3% |

Others | 4 | 1.2% |

Total | 336 | 100.0% |

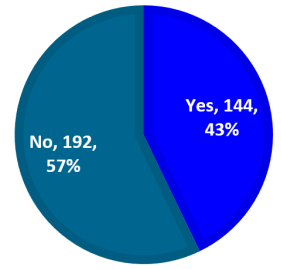

Need for Internet | Number | Percentage |

|---|---|---|

Yes | 165 | 49.1% |

No | 171 | 50.9% |

Total | 336 | 100.0% |

Level of Convenience | Number | Percentage |

|---|---|---|

Very Inconvenient | 34 | 10.1% |

Inconvenient | 20 | 6.0% |

Fair | 27 | 8.0% |

Convenient | 173 | 51.5% |

Very Convenient | 82 | 24.4% |

Total | 336 | 100.0% |

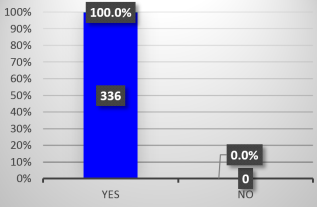

Response | Number | Percentage |

|---|---|---|

Yes | 329 | 97.9% |

No | 7 | 2.1% |

Totals | 336 | 100 |

Mobile Money | Economic Growth | ||

|---|---|---|---|

Mobile Money Usage | Pearson Correlation | 1.00 | .79** |

Sig. (2-tailed) | .001 | ||

N | 336 | 336 | |

Economic Growth | Pearson Correlation | .79** | 1.00 |

Sig. (2-tailed) | .001 | ||

N | 336 | 336 | |

**. Correlation is significant at the 0.05 level (2-tailed) | |||

Model | R | R Square | Adjusted R Square | Std. Error of the Estimate |

|---|---|---|---|---|

1 | 0.480 | 0.230 | 0.228 | 0.737 |

a. Predictors: (Constant), Mobile Money Usage | ||||

ANOVAa | ||||||

|---|---|---|---|---|---|---|

Model | Sum of Squares | df | Mean Square | F | Sig. | |

1 | Regression | 23.461 | 1 | 23.461 | 42.812 | .001b |

Residual | 183.032 | 334 | 0.548 | |||

Total | 206.492 | 335 | ||||

a. Dependent Variable: Economic Growth | ||||||

b. Predictors: (Constant), Mobile Money Usage | ||||||

Coefficientsa | ||||||

|---|---|---|---|---|---|---|

Model | Unstandardized Coefficients | Standardized Coefficients | t | Sig. | ||

B | Std. Error | Beta | ||||

1 | (Constant) | 3.105 | 0.23 | 38.869 | 0.001 | |

Mobile Money Usage | 0.339 | 0.024 | 0.48 | 14.125 | 0.001 | |

a. Dependent Variable: Economic Growth | ||||||

APIs | Application Programming Interfaces |

ATM | Automated Teller Machine |

BoU | Bank of Uganda |

CVI | Content Validity Index |

FY | Fiscal Year |

G20 | Group of Twenty |

GDP | Gross Domestic Product |

GKMA | Greater Kampala Metropolitan Area |

LDCs | Least Developed Countries |

MNOs | Mobile Network Operators |

MoFPED | Ministry of Finance, Planning and Economic Development |

MoMo | Mobile Money |

MTN | Mobile Telephone Network |

NDPIII | National Development Plan III |

NWSC | National Water and Sewerage Corporation |

PDM | Parish Development Model |

PIN | Personal Identification Number |

SPSS | Statistical Package for Social Scientists |

UBOS | Uganda Bureau of Statistics |

UCC | Uganda Communications Commission |

UEDCL | Uganda Electricity Distribution Company Limited |

UGX | Uganda Shillings |

UNCST | Uganda National Council of Science and Technology |

USSD | Unstructured Supplementary Service Data |

| [1] | Adelaja, A. O., Umeorah, S. C., Abikoye, B. E., & Nezianya, M. C. (2024). Advancing financial inclusion through fintech: Solutions for unbanked and underbanked populations. World Journal of Advanced Research and Reviews, 23(01), 427–438. |

| [2] | AFI. (2011). A Quick Guide to the Maya Declaration on Financial Inclusion. |

| [3] | Akcam, B. K., Guney, S., & Cresswell, A. M. (2019). Research design and major issues in developing dynamic theories by secondary analysis of qualitative data. Systems, 7(3), 40. |

| [4] | Arinze, E. D., Uchechukwu, A. J., & Nnachi, A. B. (2024). Mobile Money Adoption in Uganda International Digital Organization for Scientific Research Mobile Money Adoption in Uganda. (October). |

| [5] | Arvidsson, N. (2019). Money: The Greatest Innovation in the History of Humanity. |

| [6] | Asongu, S., & Odhiambo, N. (2022). The role of mobile characteristics on mobile money innovations. Quality & Quantity, 56(6), 4693–4710. |

| [7] | Bank of Uganda. (2011). Annual Report 2010/11. |

| [8] | Bank of Uganda. (2021). Annual Report. |

| [9] | Bank of Uganda. (2022). Annual Financial Stability Report. |

| [10] | Bank of Uganda. (2024). Annual Report 2023/2024. |

| [11] | Bank of Uganda, & MoFPED. (2023). National Financial Inclusion Strategy (2023-2028) (pp. 3–100). |

| [12] | Bank of Uganda. (2023). The Republic of Uganda National Financial Inclusion Strategy. (November), 1–100. |

| [13] | Campbell, S., Greenwood, M., Prior, S., Shearer, T., Walkem, K., Young, S., Bywaters, D., & Walker, K. (2020). Purposive sampling: complex or simple? Research case examples. Journal of Research in Nursing, 25(8), 652–661. |

| [14] | Collis, J., & Hussey, R. (2014). Identifying your paradigm. In Business Research (pp. 42–57). Springer. |

| [15] | Creswell, J. W., & Poth, C. N. (2016). Qualitative inquiry and research design: Choosing among five approaches. Sage publications. |

| [16] | Félix F., S., & Muehlschlegel, T. (2023). Mobile Money, Perception about Cash, and Financial Inclusion: Learning from Uganda’s Micro-Level Data (WP/23/238). |

| [17] |

GPFI. (2017). G20 Leaders Welcomes the 2017 G20 Financial Inclusion Action Plan.

https://www.gpfi.org/news/g20-leaders-welcome-2017-g20-financial-inclusion-action-plan |

| [18] | Hochkamp, F., & Rabe, M. (2022). Outlier detection in data mining: Exclusion of errors or loss of information? Changing Tides: The New Role of Resilience and Sustainability in Logistics and Supply Chain Management–Innovative Approaches for the Shift to a New Era. Proceedings of the Hamburg International Conference of Logistics (HICL), Vol. 33, 91–117. |

| [19] | IMF. (2023). Mobile Money, Perception about Cash, and Financial Inclusion: Learning from Uganda’s Micro-Level Data. IMF Working Papers, 2023(238), 1. |

| [20] | Kelly, A. E., & Palaniappan, S. (2023). Using a technology acceptance model to determine factors influencing continued usage of mobile money service transactions in Ghana. Journal of Innovation and Entrepreneurship, 12(1), 34. |

| [21] | Kovacic, D. (2018). Using the content validity index to determine content validity of an instrument assessing health care providers’ general knowledge of human trafficking. Journal of Human Trafficking, 4(4), 327–335. |

| [22] | L. Haven, T., & Van Grootel, D. L. (2019). Preregistering qualitative research. Accountability in Research, 26(3), 229–244. |

| [23] | Lissah, J., Kirobo, A., & Govella, M. M. (2022). Adoption of Cashless Economy in the World: A Review. IOSR Journal of Economics and Finance, 13(2), 37–48. |

| [24] | Liu, Y., Weng, X., Wan, J., Yue, X., Song, H., & Vasilakos, A. V. (2017). Exploring data validity in transportation systems for smart cities. IEEE Communications Magazine, 55(5), 26–33. |

| [25] | Mehrotra, A., & Menon, S. (2021). Telecommunication networking changing customer profile preferences. In Proceedings of 2nd International Conference on Computation, Automation and Knowledge Management, ICCAKM 2021 (Number January 2021). |

| [26] | MFPED. (2024). Minister of Finance, Planning and Economic Development. (June), 54–58. |

| [27] | MTN. (2024). MTN Uganda Limited Salient features: (Number September). |

| [28] | Muchandigona, A. K., & Kalema, B. M. (2023). Mobile Phone-Based Money as a Tool for Financial Inclusion in Developing Countries: A Review. SSRN Electronic Journal, (January). |

| [29] | Nagaaba, N., Batamuriza, R., Basuta, J., & Owomugisha, M. (2025a). Conceptualizing digital finance as a precursor for financial inclusion and financial service usage in Uganda. Cogent Business and Management, 12(1). |

| [30] | Nan, W., Zhu, X., & Lynne Markus, M. (2021). What we know and don’t know about the socioeconomic impacts of mobile money in Sub-Saharan Africa: A systematic literature review. Electronic Journal of Information Systems in Developing Countries, 87(2), 1–22. |

| [31] | Nyimbiri, B. A. (2021). The Impact of the Mobile Money on People’s Use of Financial Services in Sub-Sahara Africa. Management Dynamics in the Knowledge Economy, 9(1), 137–146. |

| [32] | Osabutey, E. L. C., & Jackson, T. (2024). Mobile money and financial inclusion in Africa: Emerging themes, challenges and policy implications. Technological Forecasting and Social Change, 202(May), 123339. |

| [33] | Puspita, I. (2024). Impact of Digital Literacy Programs on Information Access in Rural African Communities in Indonesia. African Journal of Information and Knowledge Management, 2(1), 13–26. |

| [34] | Sharma, G. (2017). Pros and cons of different sampling techniques. International Journal of Applied Research, 3(7), 749–752. |

| [35] |

UBOS. (2017a). Statistical Abstract.

https://www.ubos.org/wp-content/uploads/publications/03_20182017_Statistical_Abstract.pdf |

| [36] |

UBOS. (2017b). Uganda National Household Survey 2016/17.

https://www.ubos.org/wp-content/uploads/publications/03_20182016_UNHS_FINAL_REPORT.pdf |

| [37] |

UBOS. (2019). Statistical Abstract.

https://www.ubos.org/wp-content/uploads/publications/01_20202019_Statistical_Abstract_-Final.pdf |

| [38] |

UBOS. (2020). Statistical Abstract.

https://www.ubos.org/wp-content/uploads/publications/11_2020STATISTICAL__ABSTRACT_2020.pdf |

| [39] |

UBOS. (2023). 2023 Statistical Abstract.

https://www.ubos.org/wp-content/uploads/publications/2023-Statistical-Abstract.pdf |

| [40] | UBOS. (2024). Revised Annual Gross Domestic Product 2023/24. |

| [41] | UCC. (2023). Annual Communications Sector Report 2023 Towards an Inclusive Digital Economy. |

| [42] | UN. (2024). Briefing Note On Uganda’s Journey to Graduating from the United Nations Least Developed Country Category. |

| [43] | Zins, A., & Weill, L. (2016). The determinants of financial inclusion in Africa. Review of Development Finance, 6(1), 46–57. |

APA Style

Kiberu, J., Musoke, H. B., Walusimbi, L. (2026). Impact of Mobile Money Usage on Economic Growth in Uganda. International Journal of Finance and Banking Research, 12(3), 60-74. https://doi.org/10.11648/j.ijfbr.20261203.11

ACS Style

Kiberu, J.; Musoke, H. B.; Walusimbi, L. Impact of Mobile Money Usage on Economic Growth in Uganda. Int. J. Finance Bank. Res. 2026, 12(3), 60-74. doi: 10.11648/j.ijfbr.20261203.11

@article{10.11648/j.ijfbr.20261203.11,

author = {Jonah Kiberu and Henry Buwule Musoke and Leonard Walusimbi},

title = {Impact of Mobile Money Usage on Economic Growth in Uganda},

journal = {International Journal of Finance and Banking Research},

volume = {12},

number = {3},

pages = {60-74},

doi = {10.11648/j.ijfbr.20261203.11},

url = {https://doi.org/10.11648/j.ijfbr.20261203.11},

eprint = {https://article.sciencepublishinggroup.com/pdf/10.11648.j.ijfbr.20261203.11},

abstract = {The proliferation of mobile money services in Uganda since 2009 has transformed the financial landscape, though limited empirical research has examined their contribution to economic growth. This study investigated the impact of mobile money usage on economic growth in Uganda, focusing on transaction efficiency, financial inclusion, employment generation, and savings mobilization. Grounded in pragmatism as the guiding research philosophy, the study employed a survey, descriptive, and correlational designs across four selected districts. The target sample comprised 385 respondents, with 336 (87.3%) successfully reached, including mobile money agents, agent bankers, commercial bank staff, telecom company representatives, fintech entrepreneurs, regulators, and end-users selected through simple random, purposive, and convenience sampling. Data collection utilized structured questionnaires, key informant interviews, and documentary review of reports from the Bank of Uganda, Uganda Bureau of Statistics, and Uganda Communications Commission. Quantitative data were analyzed using SPSS version 30 through descriptive statistics, and Pearson correlation, while qualitative data underwent thematic analysis. Results revealed that mobile money usage significantly contributes to economic growth through multiple channels: 83.6% of respondents used mobile money as their primary digital finance platform, with 92.0% engaging in daily transactions. The findings showed that a unit change in mobile money usage would result in a 0.339 change in economic growth. The study concludes that mobile money significantly drives Uganda’s economic growth by enhancing financial inclusion, transactional efficiency, remittance flows, and employment generation with a regression model: Economic Growth = 3.105 + 0.339 (Mobile Money Usage. Recommendations include expanding digital infrastructure, strengthening consumer protection against fraud, integrating mobile money with formal taxation systems, and promoting digital financial literacy programs to maximize mobile money’s contribution to Uganda’s economic growth.},

year = {2026}

}

TY - JOUR T1 - Impact of Mobile Money Usage on Economic Growth in Uganda AU - Jonah Kiberu AU - Henry Buwule Musoke AU - Leonard Walusimbi Y1 - 2026/06/29 PY - 2026 N1 - https://doi.org/10.11648/j.ijfbr.20261203.11 DO - 10.11648/j.ijfbr.20261203.11 T2 - International Journal of Finance and Banking Research JF - International Journal of Finance and Banking Research JO - International Journal of Finance and Banking Research SP - 60 EP - 74 PB - Science Publishing Group SN - 2472-2278 UR - https://doi.org/10.11648/j.ijfbr.20261203.11 AB - The proliferation of mobile money services in Uganda since 2009 has transformed the financial landscape, though limited empirical research has examined their contribution to economic growth. This study investigated the impact of mobile money usage on economic growth in Uganda, focusing on transaction efficiency, financial inclusion, employment generation, and savings mobilization. Grounded in pragmatism as the guiding research philosophy, the study employed a survey, descriptive, and correlational designs across four selected districts. The target sample comprised 385 respondents, with 336 (87.3%) successfully reached, including mobile money agents, agent bankers, commercial bank staff, telecom company representatives, fintech entrepreneurs, regulators, and end-users selected through simple random, purposive, and convenience sampling. Data collection utilized structured questionnaires, key informant interviews, and documentary review of reports from the Bank of Uganda, Uganda Bureau of Statistics, and Uganda Communications Commission. Quantitative data were analyzed using SPSS version 30 through descriptive statistics, and Pearson correlation, while qualitative data underwent thematic analysis. Results revealed that mobile money usage significantly contributes to economic growth through multiple channels: 83.6% of respondents used mobile money as their primary digital finance platform, with 92.0% engaging in daily transactions. The findings showed that a unit change in mobile money usage would result in a 0.339 change in economic growth. The study concludes that mobile money significantly drives Uganda’s economic growth by enhancing financial inclusion, transactional efficiency, remittance flows, and employment generation with a regression model: Economic Growth = 3.105 + 0.339 (Mobile Money Usage. Recommendations include expanding digital infrastructure, strengthening consumer protection against fraud, integrating mobile money with formal taxation systems, and promoting digital financial literacy programs to maximize mobile money’s contribution to Uganda’s economic growth. VL - 12 IS - 3 ER -

School of Graduate Studies, Ndejje University, Kampala, Uganda

Biography: Jonah Kiberu is a Ugandan scholar and with a PhD in Business Management (Finance) from Ndejje University, Uganda. Jonah has lectured at Muteesa 1 Royal University, Ndejje University, and Kampala University. He is a seasoned researcher and managing director of Gateway Research Centre, a socio-economic think tank in Kampala, Uganda. For more than 10 years, Kiberu has published papers, newspaper articles, policy briefs and held radio and television talkshows especially on economic policy in Uganda.

Research Fields: Economics, finance, Accounting, Digital finance, Taxation, Policy Analysis

School of Graduate Studies, Ndejje University, Kampala, Uganda

Biography: Henry Buwule Musoke is an Associate Professor and a seasoned researcher with more than 20 years’ experience in socio-economic and academic research. He has lectured at both undergraduate and graduate levels across several universities in Uganda. Dr. Henry has published several research papers in numerous international academic journals particularly in accounting, finance, business management, corporate governance, banking & credit management, and microfinance. He is the former Director of Ndejje University Graduate School.

Research Fields: Accounting & Finance, Corporate Governance, Business Management, Cooperatives, Credit Management, Small & Medium Enterprises

Principal Economist, Parliament of Uganda, Kampala, Uganda

Biography: Leonard Walusimbi is a senior researcher with more than 15 years of experience in research, policy development, and analysis. He has lectured in various universities across Uganda. Dr. Leonard is a former academic registrar of Buganda Royal Institute (Kampala). He is currently a Principal Policy Analyst at the Parliament of Uganda and a University Research Supervisor at Ndejje University (Uganda).

Research Fields: Economics, Policy Development and Analysis, Education Management, and Entrepreneurship

Information