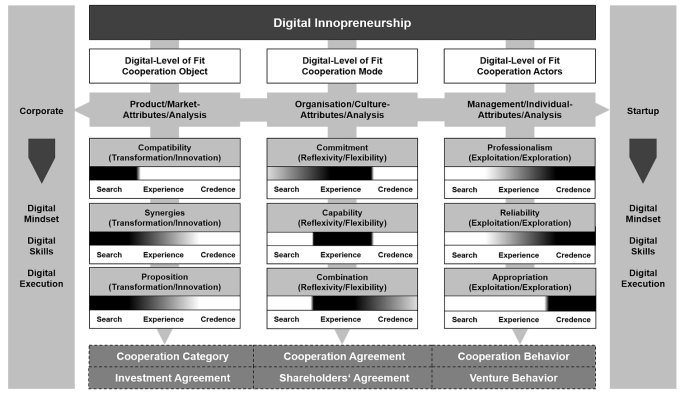

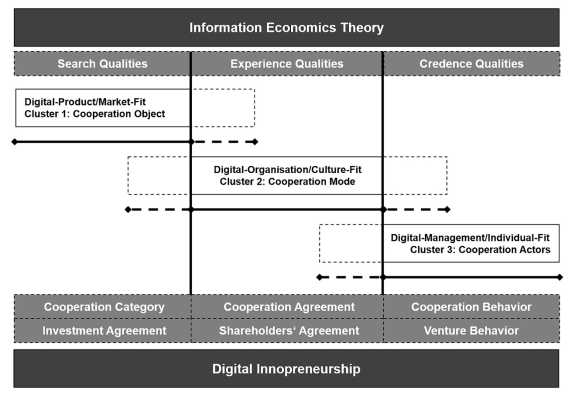

According to the previous article (Part 1), the term "Digital Innopreneurship" describes the creation of a joint digital innovation and transformation capability of startups and corporates, which is made up of the digital innovation power of startups (Digital Entrepreneurship), the digital transformation power of corporates (Digital Intrapreneurship) and the digital synergy power (Digital Interpreneurship) between these two actors. In order to unleash this power, corporates and startups must work together to shape the Digital-Innovation-Capability, Digital-Innovation-Development and Digital-Innovation-Culture in a mutually bene¬ficial way for both sides without disregarding their respective strengths and weaknesses. Against this backdrop, the players involved naturally ask themselves what such a collaboration could look like and what attributes both sides can use to check in advance whether they really fit together and which cooperation or participation model is most suitable. This article (Part 2) is intended to illustrate this conceptually and describe an initial possibility for evaluating such a cooperation between corporates and startups.

| Published in | Science Journal of Business and Management (Volume 13, Issue 2) |

| DOI | 10.11648/j.sjbm.20251302.18 |

| Page(s) | 135-154 |

| Creative Commons |

This is an Open Access article, distributed under the terms of the Creative Commons Attribution 4.0 International License (http://creativecommons.org/licenses/by/4.0/), which permits unrestricted use, distribution and reproduction in any medium or format, provided the original work is properly cited. |

| Copyright |

Copyright © The Author(s), 2025. Published by Science Publishing Group |

Digital Innopreneurship, Corporate, Startup, Cooperation, Evaluation, Information Economic Theory

| [1] | Dizdarevic, A., van de Vrande, V., & Jansen, J. (2024). When opposites attract: A review and synthesis of corporate-startup collaboration. Industry and Innovation, 31(5), 544–578. |

| [2] | Kollmann, T. (2022a). Digital Business: Grundlagen von Geschäftsmodellen und -prozessen in der digitalen Wirtschaft (8th ed.). Wiesbaden: Springer. |

| [3] | Block, J. H., Fisch, C. O., & van Praag, M. (2017). The Schumpeterian entrepreneur: A review of the empirical evidence on the antecedents, behaviour and consequences of innovative entrepreneurship. Industry and Innovation, 24(1), 61–95. |

| [4] | Kollmann, T. (2022b). Digital Entrepreneurship: Grundlagen der Unternehmensgründung in der digitalen Wirtschaft (8th ed.). Wiesbaden: Springer. |

| [5] | Kuckertz, A. (2017). Management: Corporate Entrepreneurship. Wiesbaden: Springer. |

| [6] | Kollmann, T., Hirschfeld, A., Gilde, J., Walk, V., & Pröpper, A. (2023a). Deutscher Startup Monitor 2023. Retrieved from |

| [7] | Guo, C., & Acar, M. (2005). Understanding collaboration among nonprofit organizations: Combining resource dependency, institutional, and network perspectives. Nonprofit and Voluntary Sector Quarterly, 34, 340–361. |

| [8] | Hora, W., Gast, J., Kailer, N., Rey-Marti, A., & Mas-Tur, A. (2018). David and Goliath: Causes and effects of coopetition between startups and corporates. Review of Managerial Science, 12(2), 411–439. |

| [9] | Kollmann, T. (2006). What is E-Entrepreneurship? Fundamentals of company founding in the net economy. International Journal of Technology Management, 33(4), 322–340. |

| [10] | Kollmann, T., & Jung, P. B. (2022). What is Digital Entrepreneurship? Fundamentals of company founding in the Digital Economy. In M. Keyhani, T. Kollmann, A. Ashjari, A. Sorgner, & C. E. Hull (Eds.), Handbook of Digital Entrepreneurship (pp. 27–48). Edward Elgar Publishing Ltd. |

| [11] | Baker, T., & Nelson, R. E. (2005). Creating something from nothing: Resource construction through entrepreneurial bricolage. Administrative Science Quarterly, 50(3), 329–366. |

| [12] | Christensen, C. M., McDonald, R., Altman, E. J., & Palmer, J. E. (2018). Disruptive innovation: An intellectual history and directions for future research. Journal of Management Studies, 55(7), 1043–1078. |

| [13] | Teece, D. J., Peteraf, M., & Leih, S. (2016). Dynamic capabilities and organizational agility: Risk, uncertainty, and strategy in the innovation economy. California Management Review, 58(4), 13–35. |

| [14] | Kohli, R., & Melville, N. P. (2019). Digital innovation: A review and synthesis. Information Systems Journal, 29(1), 200–223. |

| [15] |

Engels, B., & Röhl, K.-H. (2020). Cooperation of startups and SMEs in Germany: Chances, challenges, and recommendations. Econstor.

https://www.econstor.eu/bitstream/10419/224772/1/1733925406.pdf |

| [16] | Kollmann, N. (2025). Corporate-Startup-Collaboration: A Decision-Making Framework based on Information Economics Theory. Lisbon: Nova School of Business and Economics. |

| [17] | Oakey, R. P. (1993). Predatory networking: The role of small firms in the development of the British biotechnology industry. International Small Business Journal, 11(4). |

| [18] | Giglio, C., Corvello, V., Coniglio, I. M., Kraus, S., & Gast, J. (2023). Cooperation between large companies and startups: An overview of the current state of research. European Management Journal, 41(4), 551–563. |

| [19] | Zahra, S. A. (1996). Technology strategy and new venture performance: A study of corporate-sponsored and independent biotechnology ventures. Journal of Business Venturing. |

| [20] | Sorrentino, M., & Williams, M. L. (1995). Relatedness and corporate venturing: Does it really matter? Journal of Business Venturing, 10(1), 59–73. |

| [21] | Colombo, M. G., Grilli, L., & Piva, E. (2006). In search of complementary assets: The determinants of alliance formation of high-tech startups. Research Policy, 35(8), 1166–1199. |

| [22] | Dushnitsky, G., & Shaver, J. M. (2009). Limitations to interorganizational knowledge acquisition: The paradox of corporate venture capital. Strategic Management Journal, 30(10), 1045–1064. |

| [23] | Chesbrough, H. (2000). Designing corporate ventures in the shadow of private venture capital. California Management Review, 42(3), 31–49. |

| [24] | Maula, M., Autio, E., & Murray, G. (2005). Corporate venture capitalists and independent venture capitalists: What do they know, who do they know and should entrepreneurs care? Venture Capital, 7(1), 3–21. |

| [25] | Dushnitsky, G. (2008). Corporate venture capital: Past evidence and future directions. The Oxford Handbook of Entrepreneurship. |

| [26] | Kurpjuweit, S., & Wagner, S. M. (2020). Startup supplier programs: A new model for managing corporate-startup partnerships. California Management Review, 62(3). |

| [27] | Demir, F., & Lukes, M. (2024). Corporate-startup collaboration: A managerial decision-making framework based on a systematic literature review. Review of Managerial Science, 1–32. |

| [28] | Haarmann, L., Machon, F., Rabe, M., Asmar, L., & Dumitrescu, R. (2023). Venture client model: A systematic literature review. Proceedings of the European Conference on Innovation and Entrepreneurship, ECIE, 1. |

| [29] | Mais, B., Weiss, L., & Kanbach, D. (2023). Performing open innovation through strategic venture clienting: A guiding principles framework. ISPIM Conference Proceedings, 1–16. |

| [30] |

Gimmy, G., Kanbach, D., Stubner, S., König, A., & Enders, A. (2017). What BMW’s corporate VC offers that regular investors can’t. Harvard Business Review, July 27.

https://hbr.org/2017/07/what-bmws-corporate-vc-offers-that-regular-investors-cant |

| [31] | Siota, J., Alunni, A., Riveros-Chacon, P., & Wilson, M. (2020). Corporate venturing: Insights for European leaders in government, university and industry. |

| [32] | Weiblen, T., & Chesbrough, H. W. (2015). Engaging with startups to enhance corporate innovation. California Management Review, 57(2), 66–90. |

| [33] | Minshall, T., Mortara, L., Valli, R., & Probert, D. (2010). Making ‘asymmetric’ partnerships work. Research-Technology Management, 53(3), 53–63. |

| [34] | Kanbach, D. K., & Stubner, S. (2016). Corporate accelerators as a recent form of startup engagement: The what, the why, and the how. Journal of Applied Business Research, 32(6), 1761–1776. |

| [35] | Moschner, S. L., Fink, A. A., Kurpjuweit, S., Wagner, S. M., & Herstatt, C. (2019). Toward a better understanding of corporate accelerator models. Business Horizons, 62(5), 637–647. |

| [36] | Sykes, H. B. (1990). Corporate venture capital: Strategies for success. Journal of Business Venturing, 5(1), 37–47. |

| [37] | Chesbrough, H., & Tucci, C. L. (2002). Corporate venture capital in the context of corporate innovation. Ecole Poly-technique Fédérale de Lausanne. Retrieved from |

| [38] | Basu, S., Phelps, C., & Kotha, S. (2011). Towards understanding who makes corporate venture capital investments and why. Journal of Business Venturing, 26(2), 153–171. |

| [39] | Reh, S., Jarvinen, T., & Noell, F. (2021). Why the Golden Age of Corporate Venture Capital is yet to come – despite COVID-19. Retrieved from |

| [40] | Dushnitsky, G., & Lenox, M. J. (2006). When does corporate venture capital investment create firm value? Journal of Business Venturing, 21(6), 753–772. |

| [41] | Kohler, T. (2016). Corporate accelerators: Building bridges between corporations and startups. Business Horizons, 59(3), 347–357. |

| [42] | Rothaermel, F. T. (2001). Complementary assets, strategic alliances, and the incumbent’s advantage: An empirical study of industry and firm effects in the biopharmaceutical industry. Research Policy, 30(8), 1235–1251. |

| [43] | Stuart, T. E., Hoang, H., & Hybels, R. C. (1999). Interorganizational endorsements and the performance of entrepreneurial ventures. Administrative Science Quarterly, 44(2), 315–349. |

| [44] | Bauer, S., Obwegeser, N., & Avdagic, Z. (2016). Corporate accelerators: Transferring technology innovation to incumbent companies. MCIS 2016 Proceedings, 57. |

| [45] | Cohen, S. (2013). What do accelerators do? Insights from incubators and angels. Innovations: Technology, Governance, Globalization, 8(3–4), 19–25. |

| [46] | Hakim, A. I., Sukimi, M. F., & Ab Rahman, A. H. (2024). Exploring the role of business incubators to sustainable startups: A systematic literature review. PaperASIA, 40(5b), 307–320. |

| [47] | Yusubova, A., Andries, P., & Clarysse, B. (2019). The role of incubators in overcoming technology ventures’ resource gaps at different development stages. R&D Management, 49, 803–818. |

| [48] | Malik, Muhammad Faizan, Melati Ahmad Anuar, Shehzad Khan, and Faisal Khan. 2014. “Mergers and Acquisitions: A Conceptual Review.” International Journal of Accounting and Financial Reporting 1 (1): 520. |

| [49] | Moschner, S. L., & Herstatt, C. (2017). All that glitters is not gold: How motives for open innovation collaboration with startups diverge from action in corporate accelerators. Working Papers 102, Hamburg University of Technology (TUHH), Institute for Technology and Innovation Management. |

| [50] | Shankar, R. K., & Shepherd, D. A. (2019). Accelerating strategic fit or venture emergence: Different paths adopted by corporate accelerators. Journal of Business Venturing, 34(5), 1–1. |

| [51] | Urbaniec, M., & Żur, A. (2020). Business model innovation in corporate entrepreneurship: Exploratory insights from corporate accelerators. International Entrepreneurship and Management Journal, 17, 865–888. |

| [52] | Carbone, P. (2011). Acquisition integration models: How large companies successfully integrate startups. Technology Innovation Management Review, 1(1), 26–31. |

| [53] | Kim, D. (2022). Startup acquisitions, relocation, and employee entrepreneurship. Strategic Management Journal, 43(11), 2189–2216. |

| [54] | Benson, D., & Ziedonis, R. (2010). Corporate venture capital and the returns to acquiring portfolio companies. Journal of Financial Economics, 98(3), 478–499. |

| [55] | Ademi, P., Schuhmacher, M., & Zacharakis, A. (2022). How do corporate venture capitalists evaluate digital technology ventures? A conjoint analysis. Academy of Management Proceedings, 2022(1). |

| [56] | Masucci, M., Parker, S. C., Brusoni, S., & Camerani, R. (2021). How are corporate ventures evaluated and selected? Technovation, 99(January), 102126. |

| [57] | Brandt, L., Laibach, N., Kamrath, C., & Bröring, S. (2023). Startup selection criteria for corporate venturing: What matters for incumbents? International Journal of Entrepreneurial Venturing, 15(4), 427–442. |

| [58] | Henderson, J. (2009). The role of corporate venture capital funds in financing biotechnology and healthcare: Differing approaches and performance consequences. International Journal of Technoentrepreneurship, 2(1), 29–44. |

| [59] | Lantz, J. S., Sahut, J. M., & Teulon, F. (2011). What is the real role of corporate venture capital? International Journal of Business, 16(4). |

| [60] | Andersson, M., & Xiao, J. (2016). Acquisitions of startups by incumbent businesses: A market selection process of “high-quality” entrants? Research Policy, 45(1), 1–14. |

| [61] | Weber, C., Raibulet, V., & Bauke, B. (2016). The process of relational rent generation in corporate venture capital in-vestments. International Journal of Entrepreneurial Venturing, 8(1), 62–83. |

| [62] | Kollmann, T., & Kuckertz, A. (2009). Zur Dynamik von Such-, Erfahrungs- und Vertrauenseigenschaften in komplexen Transaktionsprozessen – Eine empirische Studie am Beispiel des Venture-Capital-Investitionsprozesses. Zeitschrift für Management, 4(1), 53–74. |

| [63] | Izzo, F. (2017). Large companies and startups: South Italy’s delay. Some remarks to comment a book by Varaldo, Scarrà and Remondino. Rivista economica del Mezzogiorno, (4), 1103–1122. |

| [64] | Wessendorf, C. P., Kegelmann, J., & Terzidis, O. (2019). Determinants of early-stage technology venture valuation by business angels and venture capitalists. International Journal of Entrepreneurial Venturing, 11(5), 489–520. |

| [65] | Kollmann, T. (2022c). Digital Leadership: Grundlagen der Unternehmensführung in der digitalen Wirtschaft (2nd ed.). Wiesbaden: Springer. |

| [66] | Ma, S. (2020). The life cycle of corporate venture capital. Review of Financial Studies, 33(1), 358–394. |

| [67] | Bruno, A. V., McQuarrie, E. F., & Torgrimson, C. G. (1992). The evolution of new technology ventures over 20 years: Patterns of failure, merger, and survival. Journal of Business Venturing, 7(4), 291–302. |

| [68] | Enkel, E., & Sagmeister, V. (2020). External corporate venturing modes as a new way to develop dynamic capabilities. Technovation, 96–97. |

| [69] | Astuti, T., Helmi, A., & Riyono, B. (2023). Differences in organizational behavior amongst startup and established company: A literature review. Buletin Psikologi. |

| [70] | Feldman, M., Ozcan, S., & Reichstein, T. (2020). Variation in organizational practices: Are startups really different? Journal of Evolutionary Economics, 31, 1–31. |

| [71] | Freeman, C. (1991). Networks of innovators: A synthesis of research issues. Research Policy, 20, 499–514. |

| [72] | Rank, O. (2008). Formal structures and informal networks: Structural analysis in organizations. Scandinavian Journal of Management, 24, 145–161. |

| [73] | Camarinha-Matos, L., Afsarmanesh, H., Galeano, N., & Molina, A. (2009). Collaborative networked organizations: Concepts and practice in manufacturing enterprises. Computers & Industrial Engineering, 57(1), 46–60. |

| [74] | Baxter, J. (1975). Communication problems in large organizations. Journal of Technical Writing and Communication, 5(4), 301–304. |

| [75] | Winkel, J. (2007). Growing large while staying small: Spinning-off as an organizational strategy. |

| [76] | Kanter, R. M. (1985). Supporting innovation and venture development in established companies. Journal of Business Venturing, 1, 47–60. |

| [77] | Douglas, S., Berthod, O., Groenleer, M., & Nederhand, J. (2020). Pathways to collaborative performance: Examining the different combinations of conditions under which collaborations are successful. Policy and Society, 39(5), 638–658. |

| [78] | O'Leary, R., Choi, Y., & Gerard, C. M. (2012). The skill set of the successful collaborator. Public Administration Re-view, 72(s1), S70–S83. |

| [79] | Cao, M., & Zhang, Q. (2011). Supply chain collaboration: Impact on collaborative advantage and firm performance. Journal of Operations Management, 29(3), 163–180. |

| [80] | Oh, J., Cho, N., Kim, H., Min, Y., & Kang, S. (2011). Dynamic execution planning for reliable collaborative business processes. Information Sciences, 181, 351–361. |

| [81] | Westphal, I., Thoben, K., & Seifert, M. (2010). Managing collaboration performance to govern virtual organizations. Journal of Intelligent Manufacturing, 21, 311–320. |

| [82] | Sun, H., Yang, J., & Xu, L. (2009). CoBTx-Net: A model for business collaboration reliability verification. Information Systems Frontiers, 11, 257–272. |

| [83] | Crossley, J., Davies, H., Humphris, G., & Jolly, B. (2002). Generalisability: A key to unlock professional assessment. Medical Education, 36(10), 972–978. |

| [84] | Brennan, M., & Monson, V. (2014). Professionalism: Good for patients and health care organizations. Mayo Clinic Proceedings, 89(5), 644–652. |

| [85] | Simon, F., Harms, R., & Schiele, H. (2019). Managing corporate-startup relationships: What matters for entrepreneurs? International Journal of Entrepreneurial Venturing, 11(2), 164–186. |

| [86] | Leiponen, A., & Byma, J. (2009). If you cannot block, you better run: Small firms, cooperative innovation, and appropriation strategies. Research Policy, 38, 1478–1488. |

| [87] | Mohammadi, A., & Khashabi, P. (2016). Embracing the sharks: The impact of information exposure on the likelihood and quality of CVC investments. Working Paper Series in Economics and Institutions of Innovation 428, Royal Institute of Technology, CESIS - Centre of Excellence for Science and Innovation Studies. |

| [88] | Stigler, G. J. (1961). The economics of information. Journal of Political Economy, 69(3), 213–225. |

| [89] | Shapiro, C., & Varian, H. (1999). Information rules: A strategic guide to the network economy (pp. I-X, 1–352). |

| [90] | Antonelli, C. (2006). The business governance of localized knowledge: An information economics approach for the economics of knowledge. Industry and Innovation, 13(3), 227–261. |

| [91] | Nelson, P. (1970). Information and consumer behavior. Journal of Political Economy, 78(2), 311–329. |

| [92] | Darby, M. R., & Karni, E. (1973). Free competition and the optimal amount of fraud. The Journal of Law and Economics, 16(1), 67–88. |

| [93] | Adler, J. (1996). Informationsökonomische Fundierung von Austauschprozessen: Eine nachfragerorientierte Analyse. Springer. |

| [94] | Girard, T., & Dion, P. (2010). Validating the search, experience, and credence product classification framework. Journal of Business Research, 63, 1079–1087. h |

| [95] | Ford, G. T., Smith, D. B., & Swasy, J. L. (1990). Consumer skepticism of advertising claims: Testing hypotheses from economics of information. Journal of Consumer Research, 16(4), 433–441. |

| [96] | Nair, P., & Shivdas, A. (2019). Influence of price on the dynamic transformation of search, experience and credence goods. International Journal of Innovative Technology and Exploring Engineering (IJITEE), 8(8), 3071–3081. |

| [97] | Zheng, L., Bai, T., & Cross, A. (2021). Signaling information management in entrepreneurial firms' financing acquisition: An integrated signaling and screening perspective. Journal of Global Information Management, 29, 1–31. |

| [98] | Dosis, A. (2017). On signalling and screening in markets with asymmetric information. ERN: Other IO: Empirical Studies of Firms & Markets (Topic). |

| [99] | Richman, B. M. (1962). A rating scale for product innovation. Business Horizons, 5(2), 37–44. |

| [100] | Weiber, R., Kollmann, T., & Pohl, A. (2006). Das Management technologischer Innovationen. In M. Kleinaltenkamp, W. Plinke, F. Jacob, & A. Sö (Eds.), Markt- und Produktmanagement – Die Instrumente des Business-to-Business-Marketing (pp. 83–207). Wiesbaden: Springer. |

| [101] | Guo, H., Wang, C., Zhongfeng, S., & Wang, D. (2020). Technology push or market pull? Strategic orientation in business model design and digital startup performance. Journal of Product Innovation Management, 37(4), 352–372. |

| [102] | Chemla, G., Ljungqvist, A., & Habib, M. (2004). An analysis of shareholder agreements. LSN: Corporate Governance U.S. (Topic). |

| [103] | Lacave, M., & Gutiérrez, N. (2010). Specific investments, opportunism and corporate contracts: A theory of tag-along and drag-along clauses. European Business Organization Law Review, 11, 423–458. |

| [104] | De Groote, J. K., & Backmann, J. (2020). Initiating open innovation collaborations between incumbents and startups: How can David and Goliath get along? International Journal of Innovation Management, 24(2). |

| [105] | Kollmann, T., Kollmann, K., & Kollmann, N. (2023b). Artificial Leadership: Digital transformation as a leadership task between the chief digital officer and artificial intelligence. International Journal of Business Science and Applied Management, 18(1), 76–95. |

APA Style

Kollmann, T., Kollmann, N. (2025). Digital Innopreneurship 2: The Evaluation of Collaboration Between Corporates and Startups in the Digital Economy. Science Journal of Business and Management, 13(2), 135-154. https://doi.org/10.11648/j.sjbm.20251302.18

ACS Style

Kollmann, T.; Kollmann, N. Digital Innopreneurship 2: The Evaluation of Collaboration Between Corporates and Startups in the Digital Economy. Sci. J. Bus. Manag. 2025, 13(2), 135-154. doi: 10.11648/j.sjbm.20251302.18

@article{10.11648/j.sjbm.20251302.18,

author = {Tobias Kollmann and Niklas Kollmann},

title = {Digital Innopreneurship 2: The Evaluation of Collaboration Between Corporates and Startups in the Digital Economy

},

journal = {Science Journal of Business and Management},

volume = {13},

number = {2},

pages = {135-154},

doi = {10.11648/j.sjbm.20251302.18},

url = {https://doi.org/10.11648/j.sjbm.20251302.18},

eprint = {https://article.sciencepublishinggroup.com/pdf/10.11648.j.sjbm.20251302.18},

abstract = {According to the previous article (Part 1), the term "Digital Innopreneurship" describes the creation of a joint digital innovation and transformation capability of startups and corporates, which is made up of the digital innovation power of startups (Digital Entrepreneurship), the digital transformation power of corporates (Digital Intrapreneurship) and the digital synergy power (Digital Interpreneurship) between these two actors. In order to unleash this power, corporates and startups must work together to shape the Digital-Innovation-Capability, Digital-Innovation-Development and Digital-Innovation-Culture in a mutually bene¬ficial way for both sides without disregarding their respective strengths and weaknesses. Against this backdrop, the players involved naturally ask themselves what such a collaboration could look like and what attributes both sides can use to check in advance whether they really fit together and which cooperation or participation model is most suitable. This article (Part 2) is intended to illustrate this conceptually and describe an initial possibility for evaluating such a cooperation between corporates and startups.

},

year = {2025}

}

TY - JOUR T1 - Digital Innopreneurship 2: The Evaluation of Collaboration Between Corporates and Startups in the Digital Economy AU - Tobias Kollmann AU - Niklas Kollmann Y1 - 2025/06/20 PY - 2025 N1 - https://doi.org/10.11648/j.sjbm.20251302.18 DO - 10.11648/j.sjbm.20251302.18 T2 - Science Journal of Business and Management JF - Science Journal of Business and Management JO - Science Journal of Business and Management SP - 135 EP - 154 PB - Science Publishing Group SN - 2331-0634 UR - https://doi.org/10.11648/j.sjbm.20251302.18 AB - According to the previous article (Part 1), the term "Digital Innopreneurship" describes the creation of a joint digital innovation and transformation capability of startups and corporates, which is made up of the digital innovation power of startups (Digital Entrepreneurship), the digital transformation power of corporates (Digital Intrapreneurship) and the digital synergy power (Digital Interpreneurship) between these two actors. In order to unleash this power, corporates and startups must work together to shape the Digital-Innovation-Capability, Digital-Innovation-Development and Digital-Innovation-Culture in a mutually bene¬ficial way for both sides without disregarding their respective strengths and weaknesses. Against this backdrop, the players involved naturally ask themselves what such a collaboration could look like and what attributes both sides can use to check in advance whether they really fit together and which cooperation or participation model is most suitable. This article (Part 2) is intended to illustrate this conceptually and describe an initial possibility for evaluating such a cooperation between corporates and startups. VL - 13 IS - 2 ER -

Faculty of Computer Science, University of Duisburg-Essen, Essen, Germany

Nova School of Business and Economics, Carcavelos, Portugal

Information