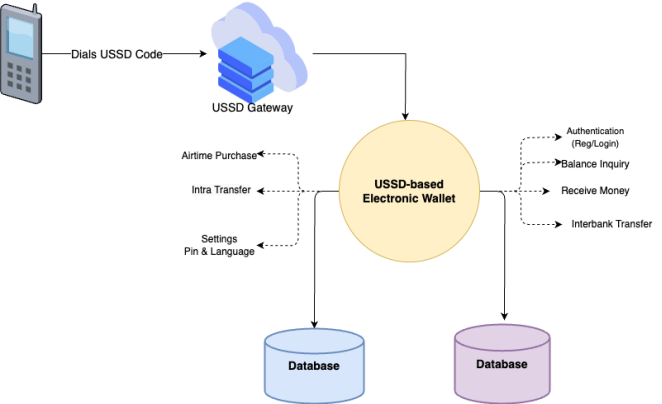

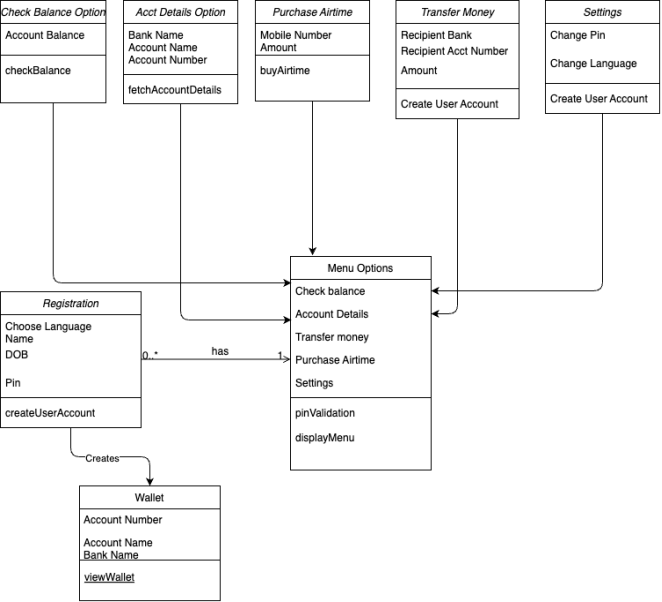

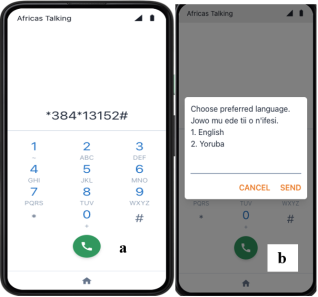

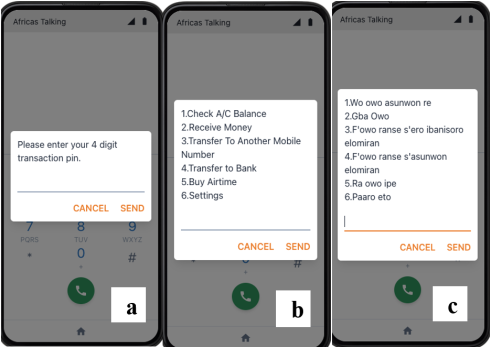

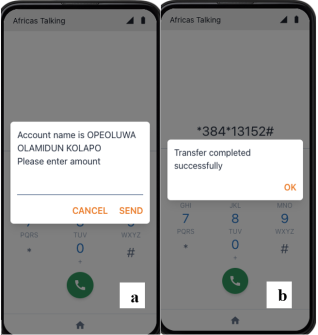

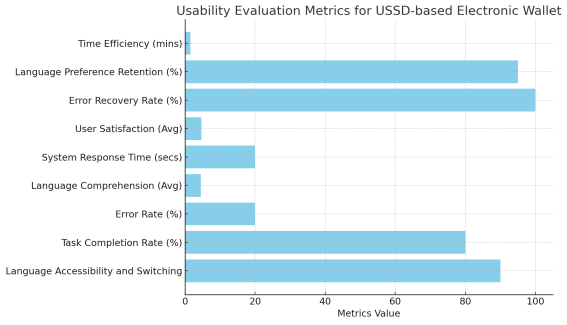

Recently, electronic wallets have emerged as a primary catalyst in driving the growth of cashless and electronic payment systems. Electronic wallets contribute to financial inclusion by providing banking services to unbanked populations and enabling easier access to financial tools without the need for physical bank branches, thereby enhancing the global shift toward cashless societies. This work designed, implemented, and evaluated a Unstructured Supplementary Service Data (USSD) based electronic wallet system aimed at promoting financial inclusion in Nigeria. The system was designed using Unified Modeling Language (UML) tools and implemented with Python, Django, PostgreSQL, and Africa’s talking. A user-centered approach was adopted, emphasizing simplicity, easy navigation, and language accessibility, with support for English and Yoruba to ensure inclusivity. Key usability testing metrics, including task completion rates, error rates, and user satisfaction, were employed to evaluate the system's effectiveness. Results indicated an 80% task completion rate, a 20% error rate, and a high user satisfaction score of 4.7 out of 5. These findings highlight the system’s capability to bridge the digital divide by providing essential financial services with no or less internet access. The USSD-based electronic wallet facilitates account creation, fund transfers, receiving payments, multilingual support and airtime purchases, making it accessible via feature phones. This study underscores the potential of USSD technology to support underserved populations, advancing financial inclusion for individuals who may lack access to smartphones or stable internet connectivity. The implementation of such a system represents a crucial step towards achieving seamless, secure financial transactions in Nigeria, ultimately fostering greater economic empowerment among marginalized communities.

| Published in | American Journal of Data Mining and Knowledge Discovery (Volume 11, Issue 1) |

| DOI | 10.11648/j.ajdmkd.20261101.12 |

| Page(s) | 8-17 |

| Creative Commons |

This is an Open Access article, distributed under the terms of the Creative Commons Attribution 4.0 International License (http://creativecommons.org/licenses/by/4.0/), which permits unrestricted use, distribution and reproduction in any medium or format, provided the original work is properly cited. |

| Copyright |

Copyright © The Author(s), 2026. Published by Science Publishing Group |

Wallet, Electronic Wallet, USSD, Internet, Financial Inclusion, Multi-lingual

Age | Gender | Occupation | Owns Smart Phone | Owns Feature Phone | Used E-wallet | Will Use USSD-based E-wallet | I am more likely to switch |

|---|---|---|---|---|---|---|---|

15-30 | Female | Trader | No | Yes | No | Yes | Strongly Agree |

15-30 | Female | Entrepreneur | No | Yes | No | Yes | Agree |

31-45 | Male | Farmer | Yes | No | No | Yes | Strongly Agree |

31-45 | Male | Farmer | No | Yes | No | Yes | Strongly Agree |

45-60 | Female | Trader | No | Yes | No | Yes | Strongly Agree |

45-60 | Male | Artisan | No | Yes | No | Yes | Agree |

Prefer Not To Say | Female | Others | No | Yes | No | Yes | Agree |

45-60 | Female | Trader | No | Yes | No | Yes | Strongly Agree |

15-30 | Male | Artisan | No | Yes | No | Yes | Agree |

31-45 | Female | Farmer | No | Yes | No | Yes | Agree |

45-60 | Female | Farmer | No | Yes | No | Yes | Strongly Agree |

15-30 | Male | Farmer | No | Yes | No | Yes | Agree |

45-60 | Male | Artisan | No | Yes | No | Yes | Agree |

45-60 | Male | Trader | No | Yes | No | Yes | Strongly Agree |

31-45 | Male | Artisan | No | Yes | No | Yes | Agree |

31-45 | Female | Entrepreneur | No | Yes | No | Yes | Agree |

45-60 | Female | Trader | No | Yes | No | Yes | Strongly Agree |

45-60 | Female | Farmer | No | Yes | No | Yes | Agree |

15-30 | Male | Farmer | No | Yes | No | Yes | Agree |

15-30 | Female | Farmer | Yes | Yes | No | Yes | Strongly Agree |

15-30 | Male | Artisan | No | Yes | No | Yes | Agree |

31-45 | Female | Others | No | Yes | No | Yes | Agree |

15-30 | Male | Trader | No | Yes | No | Yes | Agree |

31-45 | Female | Trader | No | Yes | No | Yes | Strongly Agree |

15-30 | Male | Farmer | No | Yes | No | Yes | Agree |

31-45 | Female | Others | No | Yes | No | Yes | Agree |

31-45 | Male | Trader | No | Yes | No | Yes | Agree |

31-45 | Female | Entrepreneur | No | Yes | No | No | Agree |

15-30 | Female | Farmer | No | Yes | No | Yes | Strongly Agree |

15-30 | Female | Trader | No | Yes | No | Yes | Strongly Agree |

15-30 | Male | Artisan | No | Yes | No | Yes | Strongly Agree |

15-30 | Female | Farmer | No | Yes | No | Yes | Agree |

45-60 | Male | Trader | Yes | Yes | No | No | Agree |

15-30 | Female | Farmer | No | Yes | No | Yes | Agree |

Greater than 60 | Female | Farmer | No | Yes | No | Yes | Agree |

15-30 | Male | Artisan | No | Yes | No | Yes | Agree |

31-45 | Female | Others | No | Yes | No | No | Agree |

45-60 | Male | Farmer | No | Yes | No | Yes | Agree |

31-45 | Female | Others | No | Yes | No | Yes | Agree |

15-30 | Male | Artisan | No | Yes | No | Yes | Agree |

15-30 | Male | Farmer | No | Yes | No | Yes | Agree |

31-45 | Female | Others | No | Yes | No | Yes | Agree |

45-60 | Male | Farmer | No | Yes | No | No | Agree |

31-45 | Female | Others | No | Yes | No | Yes | Agree |

45-60 | Male | Artisan | No | Yes | No | Yes | Agree |

45-60 | Male | Farmer | No | Yes | No | Yes | Agree |

31-45 | Female | Farmer | No | Yes | No | Yes | Agree |

45-60 | Male | Farmer | No | Yes | No | Yes | Agree |

31-45 | Female | Others | No | Yes | No | Yes | Agree |

15-30 | Male | Artisan | No | Yes | No | Yes | Agree |

15-30 | Male | Trader | No | Yes | No | Yes | Agree |

USSD | Unstructured Supplementary Service Data |

ARDL | Autoregressive Distributed Lag |

SPSS | Statistical Package for the Social Sciences |

ACID | Atomicity, Consistency, Isolation, Durability |

| [1] | Enhancing Financial Innovation & Access (EFInA). (2023). Access to Financial Services in Nigeria Survey 2023 (A2F): Unlocking Insights to Accelerate Financial and Economic Inclusion. Lagos, Nigeria. |

| [2] | Adewusi, O., Msagusa, W. S., Imanirumva, J. P., Obadofin, O., & Ndibwile, J. D. (2025). Hybrid USSD-based authentication for inclusive e-government mobile money services. |

| [3] | Mwale, M., & Banda, D. (2025). From disconnection to inclusion: Advancing financial services in Zambia through USSD technology. International Journal of Social Sciences, Humanities & Management Research, 4(1). |

| [4] | Aker, J. C., & Wilson, K. (2023). Mobile money and financial inclusion: The role of mobile technology in expanding access to financial services in developing economies. Information Technologies & International Development, 19, 1–16. |

| [5] | Ruslim, T. S., Herwindiati, D. E., & Cokki. (2024). Adoption of e-wallet in the post-pandemic era: A study on Generation X’s intention to use e-wallet. Innovative Marketing, 20(2), 267–280. |

| [6] |

Ujjawal, N., & Sharma, S. (2024). Adoption of mobile wallets by tourists for digital payments in India: An investigation of behavioural intention and the moderating impact of digital innovativeness. International Journal of Global Management Perspectives, 1(1), 6–21. Retrieved from

https://qtanalytics.in/journals/index.php/IJGMP/article/view/4617 |

| [7] | Tijjani, M., Besar, B. N., & Al-Shaghdari, F. M. O. (2022). Financial exclusion in Northern Nigeria: A lesson from developed countries. AFEBI Islamic Finance and Economic Review, 7(01), 45. |

| [8] | Amer, H., Anaan, G., Yousef, I., & Yousef, A. (2023). The efficiency and effectiveness of e-wallet systems in e-commerce platforms. Journal of Survey in Fisheries Sciences, 10(2S), pp. 2634–2644. |

| [9] | Anunobi S. (2024). Mitigating security vulnerabilities in offline USSD payments in non-smartphones: Enhancing user privacy. (Master’s thesis, Staffordshire University). |

| [10] | Haoyang, Z., Zhuoyi, H., Rui, L., & Yanfei, X. (2022). A blockchain-based digital wallet application with HoneyBadger-BFT consensus algorithm. pp. 3 - 8. Stanford Secure Computer Systems Group. |

| [11] | Bongani, C., & Venkata, K. R. (2023). Implementation of a mobile application that runs on USSD codes for mobile payment in network-constrained environments. International Journal of Creative Research Thoughts, pp. 3–8. |

| [12] | Patrick, M. (2023). Implementation of a service-oriented architecture for an e-wallet system for cashless transactions in the Democratic Republic of Congo. Pp. 1 - 17. |

| [13] | Ogbonlaiye, J. B., Kwanashie, M., & Olushola, O. (2025). Effect of financial inclusion on economic growth in Nigeria. International Journal of Research and Innovation in Social Science, 8(12), 3238–3257. |

| [14] | Africa’s Talking. (2025). USSD and payments APIs for mobile financial services (Product documentation). Retrieved from |

APA Style

Sholanke, T. F., Kolapo, O., Awoyelu, I. O. (2026). Development of a USSD-based Electronic Wallet System. American Journal of Data Mining and Knowledge Discovery, 11(1), 8-17. https://doi.org/10.11648/j.ajdmkd.20261101.12

ACS Style

Sholanke, T. F.; Kolapo, O.; Awoyelu, I. O. Development of a USSD-based Electronic Wallet System. Am. J. Data Min. Knowl. Discov. 2026, 11(1), 8-17. doi: 10.11648/j.ajdmkd.20261101.12

@article{10.11648/j.ajdmkd.20261101.12,

author = {Temitope Folasade Sholanke and Opeoluwa Kolapo and Iyabo Olukemi Awoyelu},

title = {Development of a USSD-based Electronic Wallet System},

journal = {American Journal of Data Mining and Knowledge Discovery},

volume = {11},

number = {1},

pages = {8-17},

doi = {10.11648/j.ajdmkd.20261101.12},

url = {https://doi.org/10.11648/j.ajdmkd.20261101.12},

eprint = {https://article.sciencepublishinggroup.com/pdf/10.11648.j.ajdmkd.20261101.12},

abstract = {Recently, electronic wallets have emerged as a primary catalyst in driving the growth of cashless and electronic payment systems. Electronic wallets contribute to financial inclusion by providing banking services to unbanked populations and enabling easier access to financial tools without the need for physical bank branches, thereby enhancing the global shift toward cashless societies. This work designed, implemented, and evaluated a Unstructured Supplementary Service Data (USSD) based electronic wallet system aimed at promoting financial inclusion in Nigeria. The system was designed using Unified Modeling Language (UML) tools and implemented with Python, Django, PostgreSQL, and Africa’s talking. A user-centered approach was adopted, emphasizing simplicity, easy navigation, and language accessibility, with support for English and Yoruba to ensure inclusivity. Key usability testing metrics, including task completion rates, error rates, and user satisfaction, were employed to evaluate the system's effectiveness. Results indicated an 80% task completion rate, a 20% error rate, and a high user satisfaction score of 4.7 out of 5. These findings highlight the system’s capability to bridge the digital divide by providing essential financial services with no or less internet access. The USSD-based electronic wallet facilitates account creation, fund transfers, receiving payments, multilingual support and airtime purchases, making it accessible via feature phones. This study underscores the potential of USSD technology to support underserved populations, advancing financial inclusion for individuals who may lack access to smartphones or stable internet connectivity. The implementation of such a system represents a crucial step towards achieving seamless, secure financial transactions in Nigeria, ultimately fostering greater economic empowerment among marginalized communities.},

year = {2026}

}

TY - JOUR T1 - Development of a USSD-based Electronic Wallet System AU - Temitope Folasade Sholanke AU - Opeoluwa Kolapo AU - Iyabo Olukemi Awoyelu Y1 - 2026/04/23 PY - 2026 N1 - https://doi.org/10.11648/j.ajdmkd.20261101.12 DO - 10.11648/j.ajdmkd.20261101.12 T2 - American Journal of Data Mining and Knowledge Discovery JF - American Journal of Data Mining and Knowledge Discovery JO - American Journal of Data Mining and Knowledge Discovery SP - 8 EP - 17 PB - Science Publishing Group SN - 2578-7837 UR - https://doi.org/10.11648/j.ajdmkd.20261101.12 AB - Recently, electronic wallets have emerged as a primary catalyst in driving the growth of cashless and electronic payment systems. Electronic wallets contribute to financial inclusion by providing banking services to unbanked populations and enabling easier access to financial tools without the need for physical bank branches, thereby enhancing the global shift toward cashless societies. This work designed, implemented, and evaluated a Unstructured Supplementary Service Data (USSD) based electronic wallet system aimed at promoting financial inclusion in Nigeria. The system was designed using Unified Modeling Language (UML) tools and implemented with Python, Django, PostgreSQL, and Africa’s talking. A user-centered approach was adopted, emphasizing simplicity, easy navigation, and language accessibility, with support for English and Yoruba to ensure inclusivity. Key usability testing metrics, including task completion rates, error rates, and user satisfaction, were employed to evaluate the system's effectiveness. Results indicated an 80% task completion rate, a 20% error rate, and a high user satisfaction score of 4.7 out of 5. These findings highlight the system’s capability to bridge the digital divide by providing essential financial services with no or less internet access. The USSD-based electronic wallet facilitates account creation, fund transfers, receiving payments, multilingual support and airtime purchases, making it accessible via feature phones. This study underscores the potential of USSD technology to support underserved populations, advancing financial inclusion for individuals who may lack access to smartphones or stable internet connectivity. The implementation of such a system represents a crucial step towards achieving seamless, secure financial transactions in Nigeria, ultimately fostering greater economic empowerment among marginalized communities. VL - 11 IS - 1 ER -

Department of Computer Science and Cybersecurity, Obafemi Awolowo University, Ile-Ife, Nigeria

Biography: Temitope Folasade Sholanke is a Lecturer at the Department of Computer Science and Cybersecurity, Obafemi Awolowo University, Ile-Ife, Nigeria. She completed her PhD in Computer Science at Obafemi Awolowo University, Ile-Ife, Nigeria in the year 2024 and Master of Computer Science from the same institution in 2015. Dr. Temitope is a member of the Nigeria Computer Society (NCS) and Nigerian Women in Information Technology (NIWIT). She had published some of her work in both local and international journals and presented in several conferences.

Research Fields: Artificial Intelligence (AI), Machine Learning, Deep Learning, Intelligent User Interfaces, Computer Vision, AI Personalized Learning Systems, Pattern Recognition and Intelligent Systems, Data Mining and Knowledge Discovery, AI for Identity Management and Human-Centered Educational Technology

Department of Computer Science and Engineering, Obafemi Awolowo University, Ile-Ife, Nigeria

Biography: Opeoluwa Kolapo is a graduate of Obafemi Awolowo University. He completed his BSc in Computer Science with Mathematics. He is a results-driven, detail-oriented Software Engineer with 5+ years’ experience in the industry. He is passionate about designing, implementing and optimizing backend architectures, and tackling complex technical challenges. He is currently the Lead Software Engineer at Woodcore, a Cloud Banking company that provides Core Banking infrastructure.

Research Fields: Backend architecture design, Mobile financial inclusion, USSD payment systems, Distributed cloud banking, Multilingual fintech design, Scalable Python development, Digital payment systems, Electronic wallet usability

Department of Computer Science and Engineering, Obafemi Awolowo University, Ile-Ife, Nigeria

Biography: Iyabo Olukemi Awoyelu is a Professor of Computer Science in the Department of Com-puter Science and Engineering, Obafemi Awolowo University, Ile-Ife, Nigeria. She teaches Database Systems, Principles and Applications of Data Mining, Techniques in Data Analysis and Principles of Compilers. She has over 20 years of teaching and research experience. Her research interests are in Data ware-housing, Data Mining, Data Analytics, Digital Transformation and Recommender Systems. She is a member of Nigeria Com-puter Society (NCS), Nigerian Women in Information Technol-ogy (NIWIT) and Computer Professionals of Nigeria (CPN). She has mentored twenty Postgraduate students and has over thirty (30) published journal articles and referred conference proceedings to her credit.

Research Fields: Data warehousing, Data Mining, Data Analytics, Artificial Intelligence, Machine Learning, Recommender Systems, Digital Transformation

Information