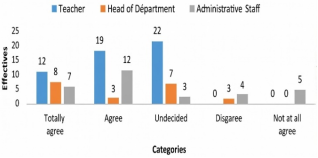

This scientific reflection questions the low sustainability of financial governance practices within the faculty institutions of the University of Yaoundé 1. The global challenges of university governance call for more virtuous management practices. This is why, in 2017, the Conference of Ministers of Education of the States and Governments of La Francophonie recommended not only the integration of sustainable financing principles into sectoral and sub-sectoral budgetary guidelines for education, but also a transformation of financial management practices in educational institutions. Today, the reality of university governance in Cameroon is quite different. Indeed, the report on medium-term expenditure planning (2020-2022) reveals that Cameroon is struggling to integrate sustainable finance practices into sectoral education governance, particularly in public higher education institutions. So why is it that state university faculties do not integrate the principles of sustainable finance into their day-to-day financial management? Taking the University of Yaoundé 1 as a case study, the methodological approach is hypothetical-deductive. The analysis combines qualitative and quantitative methods. The field survey targeted managers at three levels of intervention in the financial governance chain: institution directors and/or their deputies (N=03), department heads (N=20) and teaching and non-teaching staff (N=85). The results reveal a real lack of understanding of the principles of sustainable finance in the financial governance chain. This lack of knowledge is accompanied by insufficient consideration of extra-financial criteria, such as stakeholders and social issues, in the day-to-day financial management of the faculties of the University of Yaoundé 1.

| Published in | Innovation Business (Volume 1, Issue 1) |

| DOI | 10.11648/j.ib.20260101.12 |

| Page(s) | 21-26 |

| Creative Commons |

This is an Open Access article, distributed under the terms of the Creative Commons Attribution 4.0 International License (http://creativecommons.org/licenses/by/4.0/), which permits unrestricted use, distribution and reproduction in any medium or format, provided the original work is properly cited. |

| Copyright |

Copyright © The Author(s), 2026. Published by Science Publishing Group |

Governance, University, Financing, Sustainability, Stakeholders

Faculty | Items: Teachers are involved in the financial management of the faculty | Total | ||||

|---|---|---|---|---|---|---|

Completely agree | All right | Undecided | Disagree | I don't agree at all | ||

Flash | 0 | 0 | 16 | 26 | 19 | 61 |

ESF | 1 | 3 | 3 | 15 | 22 | 44 |

Total | 1 | 3 | 19 | 41 | 41 | 105 |

Research hypotheses | Γ | ddl | X2Cal | X2Lu | Decision |

|---|---|---|---|---|---|

HS1 | 5% | 8 | X2Cal=42.36 | X2lu=15.51 | X2Cal > X2Lu Confirm HR1 |

HS2 | 5% | 8 | X2Cal=33.47 | X2lu=15.51 | X2Cal > X2Lu Confirms HR2 |

HS3 | 5% | 8 | X2Cal=39.25 | X2lu=15.51 | X2Cal > X2Lu Confirm HR1 |

CONFEMEN | Conference of Ministers of Education of the States and Governments of the Francophonie |

SDG | Sustainable Development Goal |

| [1] | Avom, D., Gandjon, Fankem, GS 2012. Does sustainable development constitute an element of territorial attractiveness? Application to the countries of Central Africa, Market and organizations, l'harmattan, Vol 2, N 16, pp 77-102. |

| [2] | Auvray, T., Bédu, N., Granier, C., Rigot S. 2022. The finance industry, Paris, Landmarks, EditionThe Discovery, 128 pages. |

| [3] | Ballet, J., & Bazin, D. 2004. Taking environmental issues seriously: the ambiguity of the stakeholder approach, VertigeO, Electronic Journal of Environmental Sciences, Vol 5, No. 2. |

| [4] | Bank of France. 2022. Macroeconomic Conjecture Point. June 2022, Paris. |

| [5] | Bégassen D., Lambrecht, P., et al. 2022. Legal Aspects of Sustainable Finance, Brussels, Larcier 162 pages. |

| [6] | Bochatey, M. 2019. Sustainable finance, a fad or a real paradigm shift, Bachelor's thesis at HES at the Haute Ecole de Genève, 127 pages. |

| [7] | Brodin, C. 2015. Beyond aid, innovative financing, Financial Techniques and Development, Volume 4, No. 121 pp. 49-58. |

| [8] | Confemen. 2018. International Seminar on Education Financing. Sustainable Education Financing: What Strategies Should Be Considered? 25 pages. |

| [9] | Confemen. 2017. Technical report 2017. 183 pages. |

| [10] | Duval, G., Mussot, P. 2019. Sustainable finance tomorrow, Official Journal of the French Republic. |

| [11] | Presidential Decree No. 93/036 of January 19, 1993 on the administrative and academic organization of the University of Yaoundé 1. |

| [12] | Faten, B., Mbarek, S., Pallas, V. 2022. Innovating for responsible and sustainable finance, Innovations Vol 2, No. 68, pp 5-19. |

| [13] | Fonkeng, GE, Chaffi, CY, and Bomda, J. 2014. Summary of research methodology in social sciences, Yaoundé, Graphicam. |

| [14] | Frimousse, S., Peretti, JM. 2021. The contribution of green and sustainable finance to extra-financial performance, Management question(s), Flight 6 No. 36, pp 141-166. |

| [15] | Lemonnier, J. 2022. Cross-functional management: tools to promote collective intelligence, Paris, Viubert. |

| [16] | Obrecht, A., Pham, M., Spehn, D., Bremond, A. 2021. Achieving the SDGs with biodiversity, Swiss Academy of Natural Sciences (SCNAT), Forum Biodiverität Schwei. |

APA Style

Lionel, K. E. R. R. (2026). Stakeholders, Sustainable Finance and Governance in the Classical Faculties of the University of Yaoundé 1 (Cameroon). Innovation Business, 1(1), 21-26. https://doi.org/10.11648/j.ib.20260101.12

ACS Style

Lionel, K. E. R. R. Stakeholders, Sustainable Finance and Governance in the Classical Faculties of the University of Yaoundé 1 (Cameroon). Innov. Bus. 2026, 1(1), 21-26. doi: 10.11648/j.ib.20260101.12

AMA Style

Lionel KERR. Stakeholders, Sustainable Finance and Governance in the Classical Faculties of the University of Yaoundé 1 (Cameroon). Innov Bus. 2026;1(1):21-26. doi: 10.11648/j.ib.20260101.12

@article{10.11648/j.ib.20260101.12,

author = {Kana Etoundi Rene Rodrigue Lionel},

title = {Stakeholders, Sustainable Finance and Governance in the Classical Faculties of the University of Yaoundé 1 (Cameroon)},

journal = {Innovation Business},

volume = {1},

number = {1},

pages = {21-26},

doi = {10.11648/j.ib.20260101.12},

url = {https://doi.org/10.11648/j.ib.20260101.12},

eprint = {https://article.sciencepublishinggroup.com/pdf/10.11648.j.ib.20260101.12},

abstract = {This scientific reflection questions the low sustainability of financial governance practices within the faculty institutions of the University of Yaoundé 1. The global challenges of university governance call for more virtuous management practices. This is why, in 2017, the Conference of Ministers of Education of the States and Governments of La Francophonie recommended not only the integration of sustainable financing principles into sectoral and sub-sectoral budgetary guidelines for education, but also a transformation of financial management practices in educational institutions. Today, the reality of university governance in Cameroon is quite different. Indeed, the report on medium-term expenditure planning (2020-2022) reveals that Cameroon is struggling to integrate sustainable finance practices into sectoral education governance, particularly in public higher education institutions. So why is it that state university faculties do not integrate the principles of sustainable finance into their day-to-day financial management? Taking the University of Yaoundé 1 as a case study, the methodological approach is hypothetical-deductive. The analysis combines qualitative and quantitative methods. The field survey targeted managers at three levels of intervention in the financial governance chain: institution directors and/or their deputies (N=03), department heads (N=20) and teaching and non-teaching staff (N=85). The results reveal a real lack of understanding of the principles of sustainable finance in the financial governance chain. This lack of knowledge is accompanied by insufficient consideration of extra-financial criteria, such as stakeholders and social issues, in the day-to-day financial management of the faculties of the University of Yaoundé 1.},

year = {2026}

}

TY - JOUR T1 - Stakeholders, Sustainable Finance and Governance in the Classical Faculties of the University of Yaoundé 1 (Cameroon) AU - Kana Etoundi Rene Rodrigue Lionel Y1 - 2026/01/31 PY - 2026 N1 - https://doi.org/10.11648/j.ib.20260101.12 DO - 10.11648/j.ib.20260101.12 T2 - Innovation Business JF - Innovation Business JO - Innovation Business SP - 21 EP - 26 PB - Science Publishing Group UR - https://doi.org/10.11648/j.ib.20260101.12 AB - This scientific reflection questions the low sustainability of financial governance practices within the faculty institutions of the University of Yaoundé 1. The global challenges of university governance call for more virtuous management practices. This is why, in 2017, the Conference of Ministers of Education of the States and Governments of La Francophonie recommended not only the integration of sustainable financing principles into sectoral and sub-sectoral budgetary guidelines for education, but also a transformation of financial management practices in educational institutions. Today, the reality of university governance in Cameroon is quite different. Indeed, the report on medium-term expenditure planning (2020-2022) reveals that Cameroon is struggling to integrate sustainable finance practices into sectoral education governance, particularly in public higher education institutions. So why is it that state university faculties do not integrate the principles of sustainable finance into their day-to-day financial management? Taking the University of Yaoundé 1 as a case study, the methodological approach is hypothetical-deductive. The analysis combines qualitative and quantitative methods. The field survey targeted managers at three levels of intervention in the financial governance chain: institution directors and/or their deputies (N=03), department heads (N=20) and teaching and non-teaching staff (N=85). The results reveal a real lack of understanding of the principles of sustainable finance in the financial governance chain. This lack of knowledge is accompanied by insufficient consideration of extra-financial criteria, such as stakeholders and social issues, in the day-to-day financial management of the faculties of the University of Yaoundé 1. VL - 1 IS - 1 ER -

Education Management, University of Yaoundé 1, Yaoundé, Cameroon

Information